T1135 Foreign Property Reporting: 2026 Guide

The T1135 Foreign Income Verification Statement is the most-misunderstood Canadian tax form most filers have ever heard of. It is not a tax. It does not change what you owe. It is purely an information return that reports specified foreign property held during the year — but missing it triggers automatic penalties that escalate fast, and the most common trap (US-listed stocks and ETFs held in a Canadian brokerage account) catches plenty of Canadians who think their investment portfolio is "all Canadian."

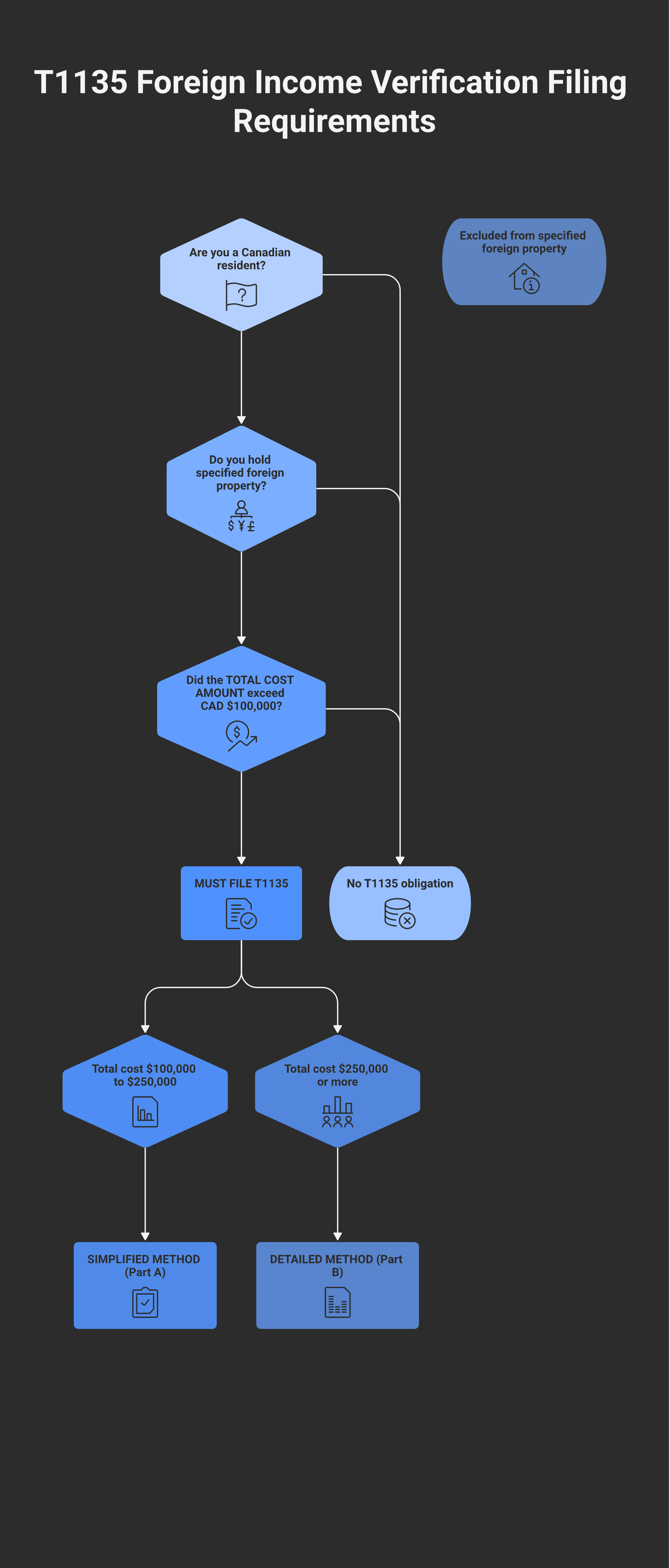

The threshold is cost amount, not market value. Once the total cost of your specified foreign property crosses CAD $100,000 at any point in the tax year — even if it has since dropped — you must file.

This guide walks through what counts under section 233.3 of the Income Tax Act, what doesn't, the simplified-versus-detailed method choice, the late-filing penalties, and the US-listed-securities-in-Canadian-brokerage trap that catches the most filers.

Key takeaways

Form T1135 must be filed if a Canadian resident's total cost of specified foreign property exceeds CAD $100,000 at any time in the tax year. The threshold is based on cost, not current market value — a portfolio that appreciated above $100K and has since dropped still requires reporting under subsection 233.3(3) of the Income Tax Act.

Two methods: simplified (Part A) for total cost between $100K and $250K — check-the-box plus top 3 countries; detailed (Part B) for total cost of $250K or more — per-property maximum cost, year-end cost, income, gains.

Registered accounts are excluded. Foreign investments inside an RRSP, FHSA, TFSA, RRIF, RESP, or RDSP do not count toward the $100K threshold, regardless of how much foreign exposure sits inside. Also excluded: personal-use property and property used in an active business.

US-listed shares and ETFs in a Canadian brokerage account are specified foreign property. What matters is the residence of the issuer, not the exchange or the currency. Apple shares held at TD Direct Investing count as foreign property. So do US-listed broad-market ETFs (VTI, VOO, QQQ, etc.).

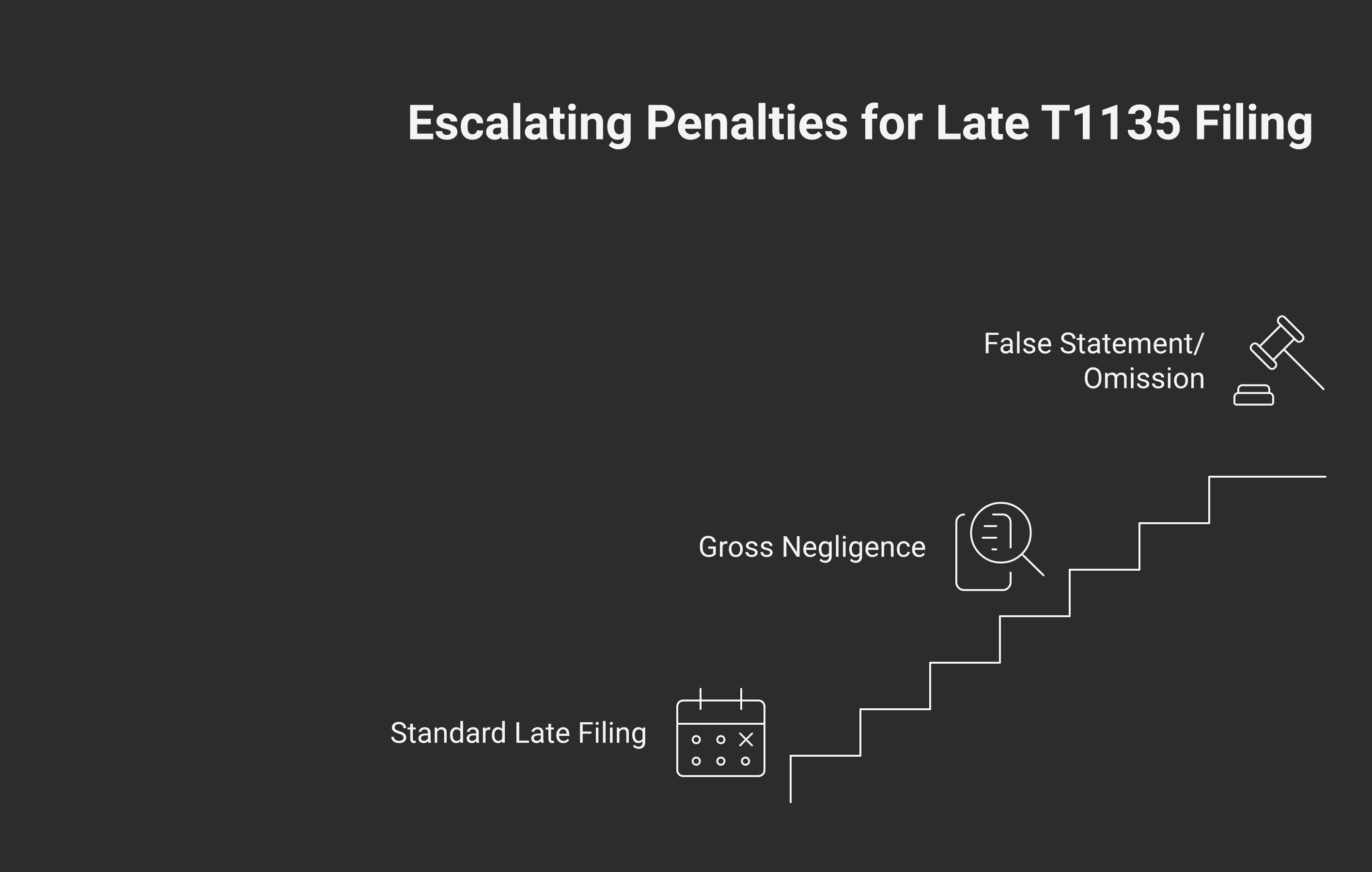

Late-filing penalty: $25 per day to a maximum of $2,500 under subsection 162(7), even if no tax is owed. If CRA determines the failure was knowing or grossly negligent, penalties escalate to $500 per month for up to 24 months ($12,000 maximum) under subsection 162(10).

What "specified foreign property" actually means

Subsection 233.3(1) of the Income Tax Act defines the term. Specified foreign property includes:

Funds or intangible property held outside Canada (a Swiss bank account, a US brokerage non-registered account, foreign currency cash above $100K of cost)

Tangible property situated outside Canada (US rental property, a vacation home in Mexico held as an investment, raw land in Belize)

Shares of non-resident corporations (Apple, Alphabet, Berkshire — even held in a Canadian-dollar TD Direct Investing account)

Interests in non-resident trusts

Interests in partnerships that own specified foreign property

Debts owed by non-residents (a personal loan to a US-resident friend, a foreign-issued bond held outside a registered account)

Rights to acquire any of the above (US-listed options, warrants, convertibles)

What is NOT specified foreign property, per subsection 233.3(1)'s exclusions:

Property held in registered Canadian accounts: RRSP, TFSA, FHSA, RRIF, RESP, RDSP, RPP, DPSP, PRPP — including any US shares, US ETFs, foreign mutual funds, foreign real estate held inside the plan

Personal-use property as defined in the Income Tax Act — a foreign vacation home that you and your family actually use, not rented out

Property used or held exclusively in carrying on an active business in Canada or abroad

Shares or debts of foreign affiliates — these are reported separately on Form T1134 (forthcoming post on T1134)

Interests in non-resident trusts acquired without consideration (a beneficiary interest in a trust set up by someone else, generally without buying in)

Australian and New Zealand retirement plan interests (specific exclusion in the statute)

The single biggest source of confusion is the registered-account exclusion. Filers see US shares in their RRSP and panic about T1135. They should not — the RRSP exemption is absolute, regardless of how foreign-heavy the holdings inside are.

The cost-amount threshold

The $100,000 trigger is based on cost amount, not market value. This matters in two ways:

Once you cross it, you file — even if values then drop. A taxpayer who held US$95K of US stocks at a cost base of CAD $130K when the position dropped triggered the obligation when they bought. If at any time during the year the total cost of specified foreign property exceeded $100K, the obligation applies for that year.

You stay under the threshold until cost crosses, even if market value is much higher. A taxpayer who bought US$50K of Apple shares 10 years ago that have grown to US$300K (CAD ~$400K market) but with CAD cost base around $65K does NOT have a T1135 obligation — cost is below $100K. (This effect tilts over time as winners accumulate and acquisition-cost positions cross thresholds.)

Cost amount is calculated in Canadian dollars, using the exchange rate at the time of acquisition. Foreign-currency-denominated assets get translated at the historical rate, not the year-end rate.

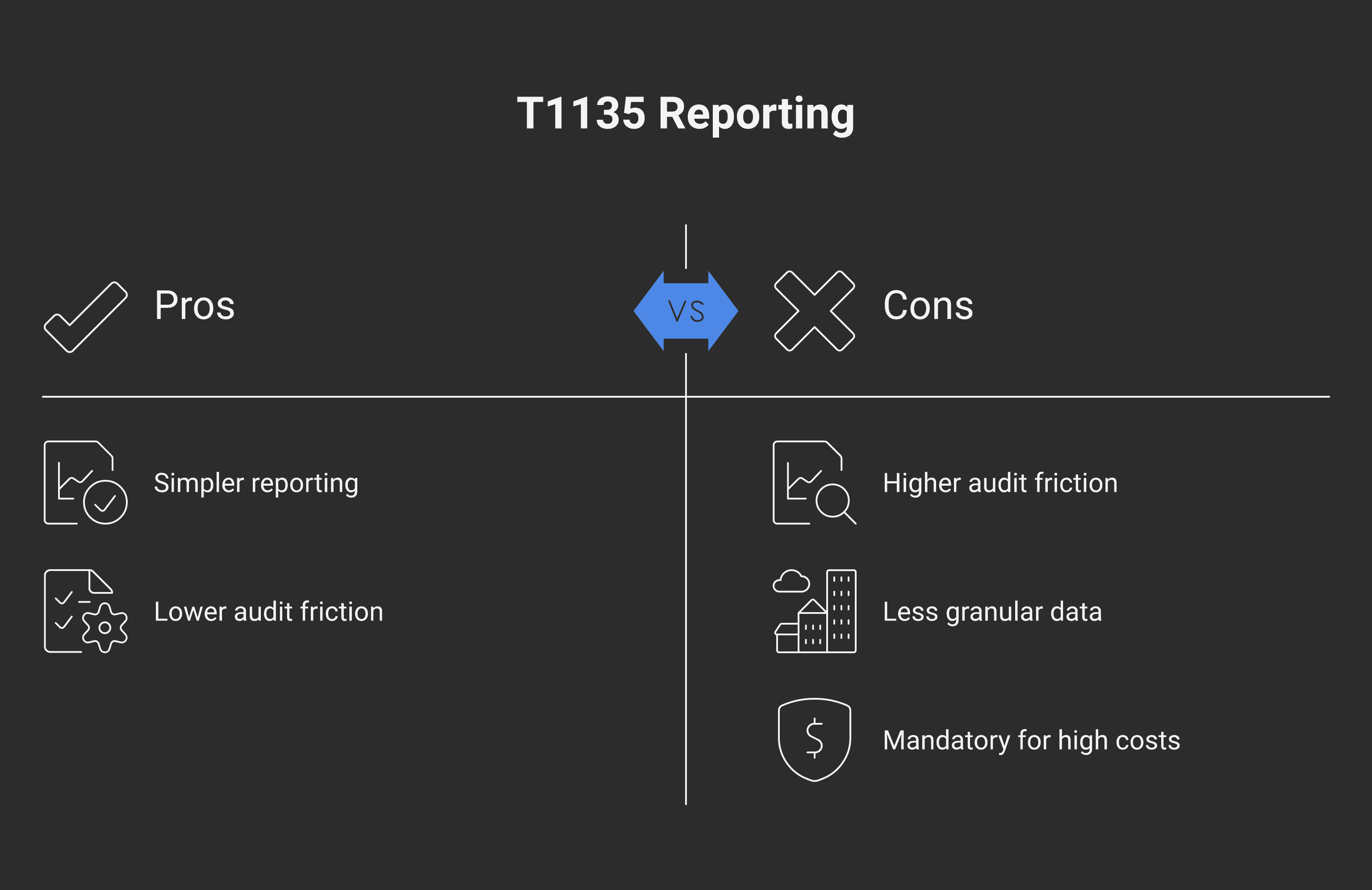

Simplified versus detailed method

Both methods report the same underlying property. The detailed version requires more granular per-asset information.

Feature | Simplified (Part A) | Detailed (Part B) |

|---|---|---|

Eligibility | Total cost $100K to $250K | Total cost $250K or more (mandatory); $100K-$250K filers may opt in |

Form sections | Check boxes per property type | Per-property maximum cost during year, cost at year-end, income, gain/loss |

Country reporting | Top 3 countries by maximum cost amount | Country-by-country per property |

Best for | Lower-complexity foreign holdings | Material foreign portfolio with multiple positions |

The simplified method is easier to complete but less informative for CRA's audit selection. The detailed method takes longer but reduces audit friction by giving CRA the full picture upfront.

The US-listed-securities trap

The single most common error a Canadian DIY investor makes is assuming that anything in a Canadian-dollar Canadian brokerage account is "Canadian property." It is not.

The rule that controls is residence of the issuer, not the exchange listing or the currency:

Apple Inc. (Apple is incorporated in Delaware, USA — resident in the US for tax purposes) — specified foreign property whether held in CAD or USD, whether listed on NASDAQ or anywhere else

Vanguard S&P 500 ETF (VOO) — a US-domiciled ETF, specified foreign property

iShares Core S&P 500 ETF (CAD-hedged) (XSP) — a Canadian-domiciled ETF that tracks the S&P 500 — NOT specified foreign property (the issuer is Canadian; the underlying exposure is foreign but doesn't count)

Royal Bank of Canada (RY) — even if held in your US-dollar account or listed on the NYSE — not specified foreign property (Canadian issuer)

This is why the "use a Canadian-domiciled wrapper" advice is consequential. A Canadian holding $200K of VOO (US-domiciled) has a T1135 obligation; the same Canadian holding $200K of VFV (Vanguard FTSE Canada All Cap, Canadian-domiciled) does not.

The brokerage statement won't tell you which is which. The clue is the ETF's domicile, available in the prospectus or on the issuer's website. Search "is [TICKER] a US-listed or Canadian-listed ETF" and verify.

Filing deadline

The T1135 is due on the same date as the T1 income tax return — April 30 for most individuals; June 15 for self-employed individuals (although taxes owing are still due April 30). Corporations file on their T2 due date — six months after fiscal year-end.

There is no extension for the T1135 specifically. The late-filing clock starts ticking on May 1 (or July 16, or six months and one day after year-end).

Late-filing penalties

The penalty structure under subsection 162(7) and section 163 of the Income Tax Act is one of the harshest in the form-filing world relative to the tax at stake:

Standard late-filing penalty:

$25 per day, starting the day after the due date

Cap: $2,500 per T1135

This applies whether or not any tax is owed — the penalty is for failure to file the information return

Gross negligence penalty (subsection 162(10)):

If CRA determines the failure was knowing or grossly negligent

$500 per month

Maximum 24 months = $12,000 per T1135

False statement or omission penalty (subsection 163(2.4)):

The greater of $24,000 and 5% of the value of unreported property

These penalties stack with any underlying tax assessment if income from the foreign property was also unreported. The Voluntary Disclosures Program (VDP) is sometimes the path forward for filers who have multi-year unfiled T1135s — but eligibility for VDP relief is narrower than it was before 2018 reforms. See our VDP guide for the current eligibility test.

Practical scenarios

Snowbird with a Florida condo. A condo used personally is exempt under the personal-use exclusion — no T1135 obligation. The same condo, rented out for any part of the year, generally becomes specified foreign property and counts toward the $100K threshold. The threshold is based on cost amount including acquisition costs and closing costs. Most Florida condos that have been rented even partially trip the obligation.

Canadian holding a US brokerage non-registered account. Every position in the account where the issuer is non-resident counts. The account itself is foreign-situated, so the cash balance also counts. Most non-registered US accounts above modest sizes trip the threshold.

Cross-border filer (US person living in Canada). US persons living in Canada have T1135 obligations on top of their US FBAR (FinCEN Form 114) and Form 8938 obligations. The two systems have similar concepts but different thresholds, different exclusions, and zero coordination. Filing both correctly requires deliberate cross-checking — one doesn't substitute for the other.

Inherited US assets. A Canadian who inherits US-listed shares from a US relative becomes the owner at the deemed cost-base of the deceased plus any step-up under US rules — but for T1135 purposes the cost amount in Canadian dollars at the date of inheritance is what's reported. A modest inheritance position can easily cross the $100K cost threshold if it includes appreciated US stock.

New immigrant with foreign assets. New immigrants to Canada get a deemed-acquisition-at-FMV step-up on becoming resident under section 128.1. That FMV becomes the T1135 cost amount going forward. The T1135 obligation only starts in the first full tax year of Canadian residence.

Practical filing tips

Pull the brokerage's annual foreign-property report. Most major Canadian brokerages now publish a year-end T1135 statement listing positions, costs, year-end values, and the country attribution. This is the cleanest starting point — but verify it against your own records, especially for ETFs (brokerages sometimes mis-classify Canadian-domiciled ETFs that hold US assets).

Use the historical exchange rate for cost amount. Convert each acquisition into CAD at the rate on the date of acquisition. Year-end conversion at the spot rate is wrong.

Track the threshold continuously, not just at year-end. The "at any time in the year" rule means a portfolio that peaked above $100K in October but ended December at $90K still triggers the filing requirement.

File even when uncertain. Where there's reasonable doubt whether the threshold was crossed, the penalty math strongly favours filing rather than not. A "no, not over the threshold" answer that turns out wrong costs $2,500-$12,000. A filed T1135 that turns out to have been unnecessary costs nothing.

For cross-border clients at Modern Axis — particularly US persons living in Canada and Canadians with US rental property — T1135 coordination with FBAR and Form 8938 is a standard part of the annual return prep. The forms ask similar questions in incompatible ways, and the penalty math on each side is harsh enough that the cost of getting it wrong dwarfs the time it takes to get it right.

Frequently asked questions

What is Form T1135 and who has to file it?

Form T1135 — the Foreign Income Verification Statement — is an information return required from Canadian residents (individuals, corporations, trusts, and partnerships) whose total cost of specified foreign property exceeded CAD $100,000 at any time in the tax year, under section 233.3 of the Income Tax Act. The form does not impose tax — it reports the property and its income. Missing it triggers penalties starting at $25 per day, capped at $2,500.

Do I have to report my RRSP, TFSA, or FHSA holdings on T1135?

No. Property held in Canadian registered accounts — RRSP, TFSA, FHSA, RRIF, RESP, RDSP, RPP, DPSP, PRPP — is specifically excluded from specified foreign property under the T1135 rules, regardless of how foreign-heavy the holdings inside the plan are. A TFSA full of US stocks does not contribute to the $100,000 threshold.

Are US stocks held in a Canadian brokerage account considered foreign property?

Yes. The rule is residence of the issuer, not the exchange or the currency. Apple shares, Microsoft shares, and US-listed ETFs (VOO, VTI, QQQ, etc.) held in a Canadian-dollar non-registered account at TD Direct Investing, Questrade, Wealthsimple, or any other Canadian brokerage are specified foreign property and count toward the $100,000 cost threshold. Canadian-domiciled ETFs that hold US assets (e.g., XSP, VFV, ZSP) are not specified foreign property.

What is the difference between the simplified and detailed T1135 method?

The simplified method (Part A) is available when total cost of specified foreign property is between $100,000 and $250,000. It requires check-box reporting of property type plus the top 3 countries by maximum cost. The detailed method (Part B) is required when total cost is $250,000 or more, and asks for per-property maximum cost during the year, year-end cost, income, and gain/loss. Filers with $100K-$250K of cost may opt in to the detailed method if it reduces audit friction.

What are the penalties for filing T1135 late?

The standard late-filing penalty under subsection 162(7) is $25 per day, capped at $2,500 per T1135. If CRA determines the failure was knowing or grossly negligent, the penalty under subsection 162(10) escalates to $500 per month for up to 24 months — a maximum of $12,000 per T1135. A separate false-statement or omission penalty under subsection 163(2.4) is the greater of $24,000 and 5% of the value of unreported property.

Does a personal-use vacation home outside Canada have to be reported?

Generally no. Personal-use property as defined in the Income Tax Act is excluded from specified foreign property. A Florida condo or French apartment that you and your family use personally — and do not rent out — does not count toward the T1135 threshold. However, the moment the property is rented (or held substantially for rental), it becomes specified foreign property and counts toward the $100,000 threshold.

When is the T1135 due?

Form T1135 is due on the same date as the related income tax return — April 30 for most individuals, June 15 for self-employed individuals (although any tax owing is still due April 30), and the T2 corporate return due date (six months after fiscal year-end) for corporations. There is no separate extension for the T1135 — the form is electronically filed alongside the income tax return.

Cross-border tax is fact-specific by nature — citizenship, residency, treaty positions, and prior filings can flip the analysis entirely. This post lays out general principles, not advice for your situation, and it cannot cover every angle that might apply to you. Speak with a Canadian and/or US tax professional who can review your full picture before relying on anything you've read here.

Alex Ataman, CPA

Founder

Modern Axis CPA