RRSP vs FHSA vs TFSA: 2026 Comparison Guide

Three tax-advantaged accounts, one decision matrix. The right answer depends on your marginal tax rate, your life stage, your time horizon, and — for the FHSA — whether you have any realistic path to a first home purchase.

The headline trade-off most articles get wrong is framing this as "RRSP versus TFSA." The actual choice in 2026 is three-way, with the FHSA carved out by the Tax-Free First Home Savings Account legislation in 2022 specifically to bridge the gap. The FHSA combines the front-end deduction of an RRSP with the back-end tax-free withdrawal of a TFSA — provided you use it for a qualifying first home. If you don't, the unused FHSA balance can transfer into your RRSP without affecting RRSP contribution room. There is no scenario where opening the FHSA hurts.

This guide walks through how each account works for 2026 under section 146 (RRSP), section 146.6 (FHSA), and section 146.2 (TFSA) of the Income Tax Act, the marginal-rate math behind picking one over another, the FHSA + Home Buyers' Plan stack toward a first home purchase, and the common mistakes.

Key takeaways

For 2026, the RRSP contribution limit is 18% of prior-year earned income up to $33,810, the FHSA annual limit is $8,000 (lifetime cap $40,000), and the TFSA dollar limit is $7,000 — total annual tax-shelter capacity of up to $48,810 for a qualifying first-time buyer.

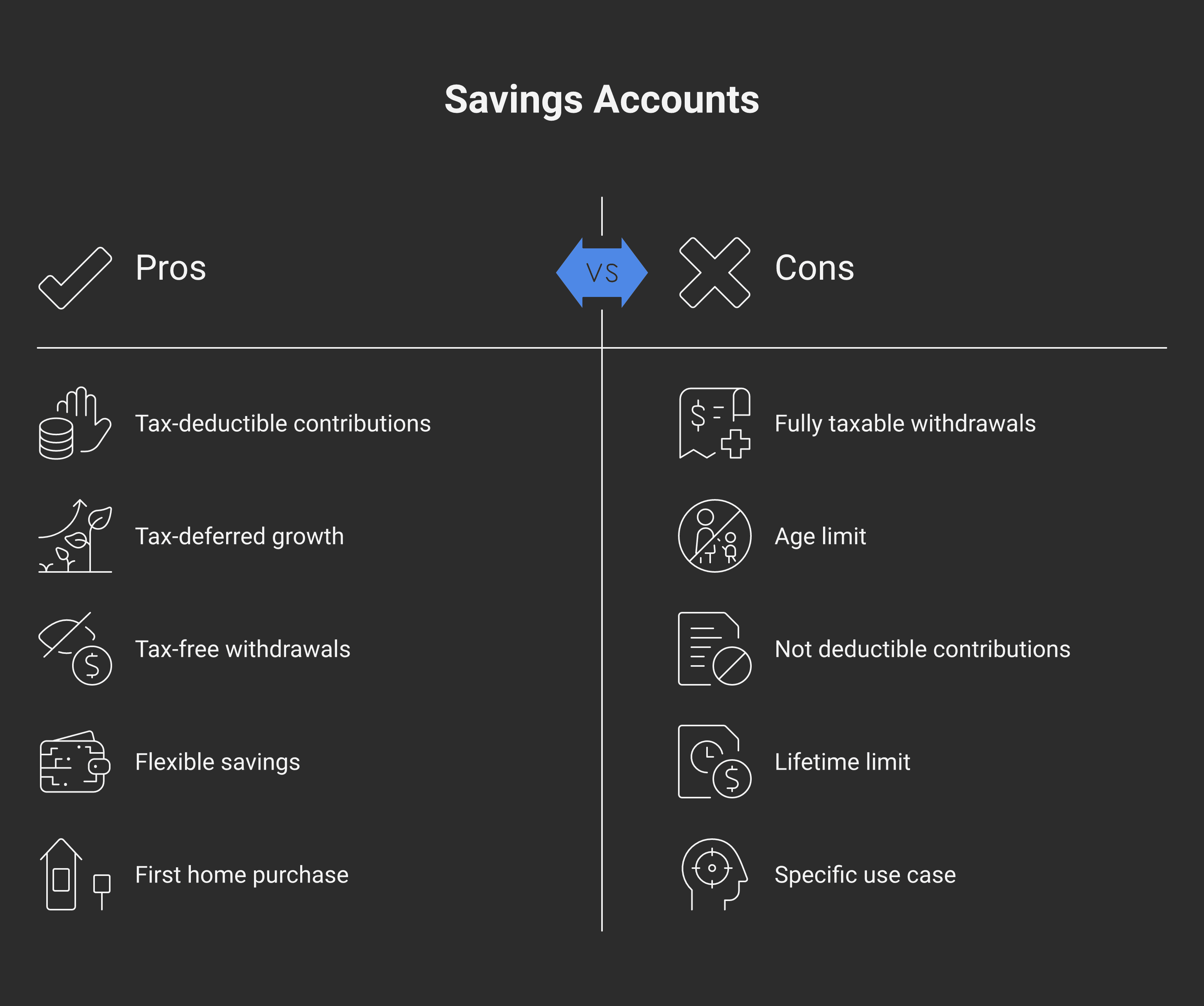

The RRSP and FHSA both give a front-end deduction. The TFSA does not. The "right" account depends on whether your marginal rate today is higher than your expected marginal rate when you withdraw — defer where future rate is lower; shelter where future rate is higher.

The FHSA is structurally dominant for first-time home savers: deductible going in (like RRSP), tax-free coming out (like TFSA), plus the unused balance can transfer to an RRSP without using RRSP room.

The FHSA + Home Buyers' Plan stack allows a first-time buyer to access up to $60,000 from RRSP (HBP, $60K cap as of April 2024) plus the full $40,000 FHSA, for $100,000 of pre-tax-favoured money toward the home — without permanent tax cost if HBP repayments are made on schedule.

Common mistake: over-contributing to a TFSA. The 1%-per-month excess contribution tax under subsection 207.02 of the Income Tax Act is the easiest tax cost to accidentally incur.

The three accounts at a glance

Feature | RRSP | FHSA | TFSA |

|---|---|---|---|

ITA section | 146 | 146.6 | 146.2 |

Year established | 1957 | 2023 | 2009 |

2026 contribution limit | 18% of earned income, capped at $33,810 | $8,000 per year ($40,000 lifetime) | $7,000 |

Contribution deductible? | Yes | Yes | No |

Growth taxed inside? | No (tax-deferred) | No (tax-free) | No (tax-free) |

Withdrawal taxed? | Yes (fully) | No (for qualifying first home) | No (anytime, any purpose) |

Carry-forward of unused room? | Yes, indefinitely | Yes, but only $8K added per year you have an FHSA | Yes, indefinitely |

Age limit | Must close by Dec 31 of year you turn 71 | Must close 15 years after opening or by Dec 31 of year you turn 71, whichever earlier | None |

Withdrawal flexibility | Restricted (without tax) — HBP, LLP, RRIF after 71 | First home only (otherwise taxable or RRSP transfer) | Anytime, anything |

RRSP — the deduction-first account

The RRSP under section 146 is the original Canadian tax-deferred retirement account, in operation since 1957. Mechanically:

Contribution is deductible from taxable income in the year contributed (or carry-forward to future years).

Investment income grows tax-deferred inside the plan.

Withdrawal is fully taxable as ordinary income, including capital gains realised inside the plan.

The math is "defer the tax until your marginal rate is lower." For most filers, that means making contributions during peak earning years (where the marginal rate is at the top of Canada's combined federal-and-provincial schedule) and withdrawing in retirement (where the marginal rate is lower because total income has dropped).

2026 contribution room. 18% of prior-year earned income, capped at the annual maximum of $33,810 for 2026 (based on $187,833 of earned income). Earned income includes employment income, self-employment income, royalties, and certain rental income. Unused contribution room carries forward indefinitely.

Spousal RRSPs. A spousal RRSP allows the higher-income spouse to contribute to a plan in which the lower-income spouse is the annuitant. Withdrawals are taxed in the annuitant's hands subject to a three-year attribution rule. Spousal RRSPs are now used less frequently than they were before pension income splitting was introduced (under section 60.03 in 2007), but remain valuable for pre-65 retirees and for spouses with significant income gaps in the early retirement years.

Home Buyers' Plan (HBP). A first-time home buyer can withdraw up to $60,000 from their RRSP under the HBP for a qualifying home purchase. The withdrawal is not taxed when made, but must be repaid to the RRSP over 15 years starting the second year after withdrawal. Missed repayments are added back to income as taxable. The HBP cap was increased from $35,000 to $60,000 in April 2024 — a significant tailwind for the FHSA + HBP stack discussed below. Buyers should also understand how the principal residence rules interact with the FHSA's "qualifying home" definition and the timing of moving in.

Lifelong Learning Plan (LLP). A second tax-free withdrawal program for full-time education, capped at $20,000 ($10,000 per year for up to two years). Repayment is over 10 years.

RRIF conversion. RRSPs must be wound up by December 31 of the year the holder turns 71 — typically by converting to a Registered Retirement Income Fund (RRIF), which then pays minimum annual amounts based on age.

FHSA — the deduction + tax-free withdrawal hybrid

The FHSA, introduced under section 146.6 by Budget 2022 and operational starting April 1, 2023, is a hybrid account designed specifically to bridge the gap between the RRSP and the TFSA for first-time home buyers.

The structural genius of the FHSA: deductible going in (like RRSP) + tax-free coming out (like TFSA) for a qualifying first home.

Eligibility. To open an FHSA you must be a Canadian resident, at least 18 years old (in some provinces, 19), and a "first-time home buyer" — meaning you did not own a home you occupied as your principal residence in the current calendar year or any of the preceding four calendar years.

Contribution limits. $8,000 per year, $40,000 lifetime cap. Unused contribution room carries forward — but only $8,000 of carry-forward room is added per year you have an FHSA open. Maximum carry-forward room is $8,000 at any time. So if you open the FHSA in year 1 and contribute zero, you have $8,000 room in year 2; contribute zero in year 2 and you have $16,000 room in year 3 (the $8K from year 2 + $8K for year 3, but capped at $16K — i.e., next year's room is forfeited).

Qualifying withdrawal — tax-free. A qualifying withdrawal under subsection 146.6(1) requires:

The individual is a first-time home buyer at the time of withdrawal

Has a written agreement to buy or build a qualifying home in Canada

Intends to occupy the home as their principal residence within one year of acquisition

When all conditions are met, the withdrawal is tax-free (the entire FHSA balance can be withdrawn at once or in stages).

Non-qualifying withdrawal. A withdrawal that does not meet the qualifying conditions is taxable as ordinary income.

FHSA → RRSP transfer. This is the FHSA's structural insurance: if you don't end up buying a home, the FHSA balance can transfer to your RRSP at any time before the 15-year FHSA closing deadline, without using RRSP contribution room. You preserve the tax deduction already taken on the FHSA contributions, defer the tax to retirement, and lose nothing.

FHSA closing rules. The FHSA must be closed by December 31 of the 15th year after opening, or by December 31 of the year the holder turns 71, whichever is earlier. Any balance remaining at closing is added to taxable income unless transferred to an RRSP.

TFSA — the tax-free anything account

The TFSA under section 146.2 is the simplest account of the three:

Contribution is not deductible.

Investment income grows tax-free.

Withdrawal is tax-free at any time, for any purpose.

Contribution room. The annual TFSA dollar limit for 2026 remains $7,000 — unchanged from 2024 and 2025 because the indexed value has not yet crossed the rounding threshold to bump to $7,500 (the next increase is expected in 2027). Cumulative contribution room for a Canadian resident who turned 18 in 2009 and has been resident since reaches approximately $109,000 in 2026.

Withdrawal mechanic. Any amount withdrawn from a TFSA is added back to the next calendar year's contribution room. This is the feature that makes the TFSA exceptional for variable-purpose savings — emergency funds, near-term home down payments, opportunistic investing. (For BC residents weighing the TFSA against direct real-estate investment, see our BC investor playbook for the broader tradeoff.)

Excess contribution tax. The single most common TFSA mistake is over-contributing. Under subsection 207.02 of the Income Tax Act, any amount contributed beyond the available room is subject to a 1% per month tax until withdrawn. CRA's My Account is the authoritative source for contribution room — but it lags by several months and is often wrong. Best practice: track contributions yourself and verify against CRA's published figure each year.

The marginal-rate decision

If you don't need the FHSA (you already own a home, or have no first-home purchase plan), the RRSP-vs-TFSA decision reduces to a single comparison:

Defer the tax to a year when your marginal rate is lower → RRSP.

Shelter the income from tax now (rate is already low or future will be similar) → TFSA.

A simplified illustration for a top-bracket Ontario resident in 2026 (top combined rate 53.53%) versus the same person in retirement at the 14% federal + ~5% provincial = 19% combined rate:

Scenario | RRSP outcome | TFSA outcome |

|---|---|---|

Contribute $10K today at 53.53% marginal rate | Refund of $5,353 (effectively $4,647 net cost) | No refund ($10K full cost) |

$10K grows to $30K over 20 years | All $30K taxable on withdrawal | All $30K tax-free |

Withdrawal taxed at 19% in retirement | $30K × 19% = $5,700 of tax → $24,300 net | $0 tax → $30,000 net |

RRSP net benefit | $24,300 net + $5,353 refund = $29,653 | $30,000 net |

If you can confidently project a lower marginal rate at withdrawal, RRSP wins. If your future marginal rate will be similar to or higher than today's, TFSA wins. Most filers in the middle of their career underestimate the rate they'll face in retirement (especially with CPP, OAS, and a corporate pension stacking on top of RRIF withdrawals), which is why the TFSA tends to be the better default for filers in middle brackets unless the marginal-rate gap is wide.

The FHSA + HBP stack toward a first home

For a first-time home buyer, the combined power of the FHSA and the Home Buyers' Plan is the single largest tax-advantaged stack available in Canadian personal finance:

FHSA: Up to $40,000 over five years (or four years if maximising early), withdrawn tax-free for the qualifying home purchase

HBP: Up to $60,000 from RRSP, tax-deferred (must be repaid over 15 years starting the second year after withdrawal)

That's up to $100,000 of pre-tax-favoured money available toward a first home — with the FHSA portion permanently tax-free if used qualifying, and the HBP portion deferred so long as repayments are made on schedule.

For a couple, both first-time buyers, the stack doubles: $200,000 of combined tax-favoured withdrawals available toward the home, half tax-free permanently (FHSA × 2) and half tax-deferred (HBP × 2).

The order to fund:

Open the FHSA first — even if you don't contribute yet. Opening it starts your contribution room accumulation.

Fill the FHSA before the RRSP for first-home savings. FHSA contributions are deductible AND withdrawals are tax-free, dominating the RRSP for this purpose.

Then use the RRSP for the additional cushion beyond $40K. RRSP contributions are deductible, but HBP withdrawals must be repaid.

The TFSA is a backup for funds beyond the FHSA + HBP capacity, or for buyers who already have a home in their household (e.g., a relationship change).

Common mistakes

Overcontributing to a TFSA. The 1%-per-month excess contribution tax under subsection 207.02 catches people who replace a withdrawal in the same calendar year (the withdrawal doesn't add room until next year), or who rely on CRA's My Account figure (which lags real activity). Track contributions yourself.

Not opening the FHSA the year you become eligible. Even with no contribution, opening the FHSA starts your contribution room. A 30-year-old who is going to buy a home in five years and waits three years to open the FHSA forfeits $8,000 of contribution room they could have stockpiled.

Choosing the RRSP because the deduction "feels real." The RRSP deduction is real, but the tax on withdrawal is just as real. If your marginal rate at withdrawal will be similar to or higher than today's, the TFSA produces the same or better after-tax result with more flexibility.

Not transferring an FHSA to an RRSP at the deadline. If you don't buy a home and the FHSA closes (15 years from opening, or year you turn 71), and you have not transferred the balance to your RRSP, the entire balance is taxable. The transfer to RRSP can be initiated any time, but must happen before the closing date.

Using an RRSP withdrawal for a non-HBP purpose just to "access the money." A regular RRSP withdrawal triggers withholding tax (typically 30% on amounts over $15,000) and is added to income. For most filers in mid-career, an unscheduled RRSP withdrawal costs about half of every dollar withdrawn in combined tax. The TFSA is for that situation, not the RRSP.

Ignoring the spousal RRSP for non-traditional retirement timing. A spouse with significant income asymmetry pre-65 can still benefit from spousal RRSP planning, even with pension income splitting available post-65. Run the calculation when household income shifts.

Planning sequencing

A useful default-order framework for filers in their 30s and 40s:

Open the FHSA (regardless of whether you'll use it imminently) if you're a first-time buyer.

Top up the TFSA as the flexible savings vehicle — primary emergency-fund and opportunistic-investing account.

Contribute to the FHSA if a home purchase is on the 5-15 year horizon.

Contribute to the RRSP for retirement, with a marginal-rate check against the TFSA to make sure you're deferring to a lower future rate.

Consider the spousal RRSP if income asymmetry is significant.

For higher-income filers in their peak earning years, the priority order often shifts: RRSP contribution maximisation comes first (because the 53%+ deduction in top-rate provinces is hard to replicate), then TFSA, then FHSA. The right answer depends on the rate differential between today and expected withdrawal year.

For owner-managers paying themselves through a CCPC, the calculus also includes whether to use the corporation to hold investment income (incurring the investment income tax at the top corporate rate) versus paying yourself first and using personal tax-advantaged accounts. The personal account stack is usually preferred for the first $50,000-$100,000 of household savings each year — only above that does the corporate-held investment income calculation start to compete.

If you're weighing the right mix between RRSP, FHSA, and TFSA for your situation, the tax planning team at Modern Axis runs combined marginal-rate projections that account for your current bracket, your expected withdrawal-year bracket, and any DTC-driven RDSP considerations sitting in the background.

Frequently asked questions

What is the RRSP contribution limit for 2026?

The RRSP contribution limit for 2026 is 18% of prior-year earned income, capped at $33,810. This is based on $187,833 of earned income in 2025. Unused contribution room carries forward indefinitely. The deadline to contribute for the 2026 tax year is March 1, 2027 (the first 60 days of 2027), per the standard RRSP contribution-window rule.

What is the FHSA contribution limit for 2026?

The FHSA annual contribution limit is $8,000 per year with a lifetime cap of $40,000. Unused contribution room carries forward, but only $8,000 of carry-forward room is added per year you have an FHSA open (with a maximum carry-forward room of $8,000 at any time). To accumulate carry-forward room, you must open the FHSA — opening it without contributing still starts the clock.

What is the TFSA contribution limit for 2026?

The TFSA dollar limit for 2026 remains $7,000, unchanged from 2024 and 2025. The limit is indexed to inflation but rounded to the nearest $500; the indexed value has not yet crossed the threshold required to bump it to $7,500 (expected for 2027). Cumulative contribution room for a Canadian resident who turned 18 in 2009 and has been resident since reaches approximately $109,000 in 2026. Any amount withdrawn from a TFSA is added back to the next calendar year's contribution room.

Can I transfer my FHSA to an RRSP without using RRSP contribution room?

Yes. Under subsection 146.6(7) of the Income Tax Act, an FHSA balance can be transferred to an RRSP at any time before the FHSA closes, without using any of your RRSP contribution room. This is the structural insurance behind the FHSA: even if you never buy a home, you keep the deduction already taken on FHSA contributions and defer the tax to retirement via the RRSP transfer.

Can I use both the FHSA and the Home Buyers' Plan for the same home purchase?

Yes. The two programs are stackable. A single first-time buyer can withdraw the full FHSA balance (up to $40,000) tax-free for a qualifying home, plus up to $60,000 under the Home Buyers' Plan from their RRSP (tax-deferred, repaid over 15 years). A couple of two first-time buyers can combine their personal limits — up to $200,000 of total tax-favoured withdrawals toward the home.

Should I prioritise the RRSP or the TFSA?

The right answer depends on your marginal tax rate today versus your expected marginal rate when you withdraw. If your today's rate is significantly higher (typically when you're in the top federal bracket in your peak earning years), the RRSP wins because the deduction now is larger than the future tax. If today's rate is comparable to or lower than your future rate, the TFSA wins because the tax-free withdrawal is permanent. For most middle-income filers, the TFSA is the right default; high earners should prioritise the RRSP first.

What happens if I withdraw money from my TFSA and put it back in the same year?

You may trigger the excess contribution tax under subsection 207.02 of the Income Tax Act. Withdrawals do not add back to your contribution room until the next calendar year. If you withdraw $5,000 in November and re-contribute $5,000 in December of the same year (assuming you have already used all your room), the $5,000 re-contribution is an excess contribution and is taxed at 1% per month until withdrawn.

A note before you go: this post covers general principles, not your specific situation. Tax outcomes turn on facts — residency, marital status, prior contributions, employment income, prior home ownership — and an article can't capture all of that. Treat this as a starting point rather than advice to rely on, and talk to a CPA or tax lawyer about your own circumstances before making any decisions based on what you've read.

Alex Ataman, CPA

Founder

Modern Axis CPA