RDSP Canada: How Grants and Bonds Stack to $90,000

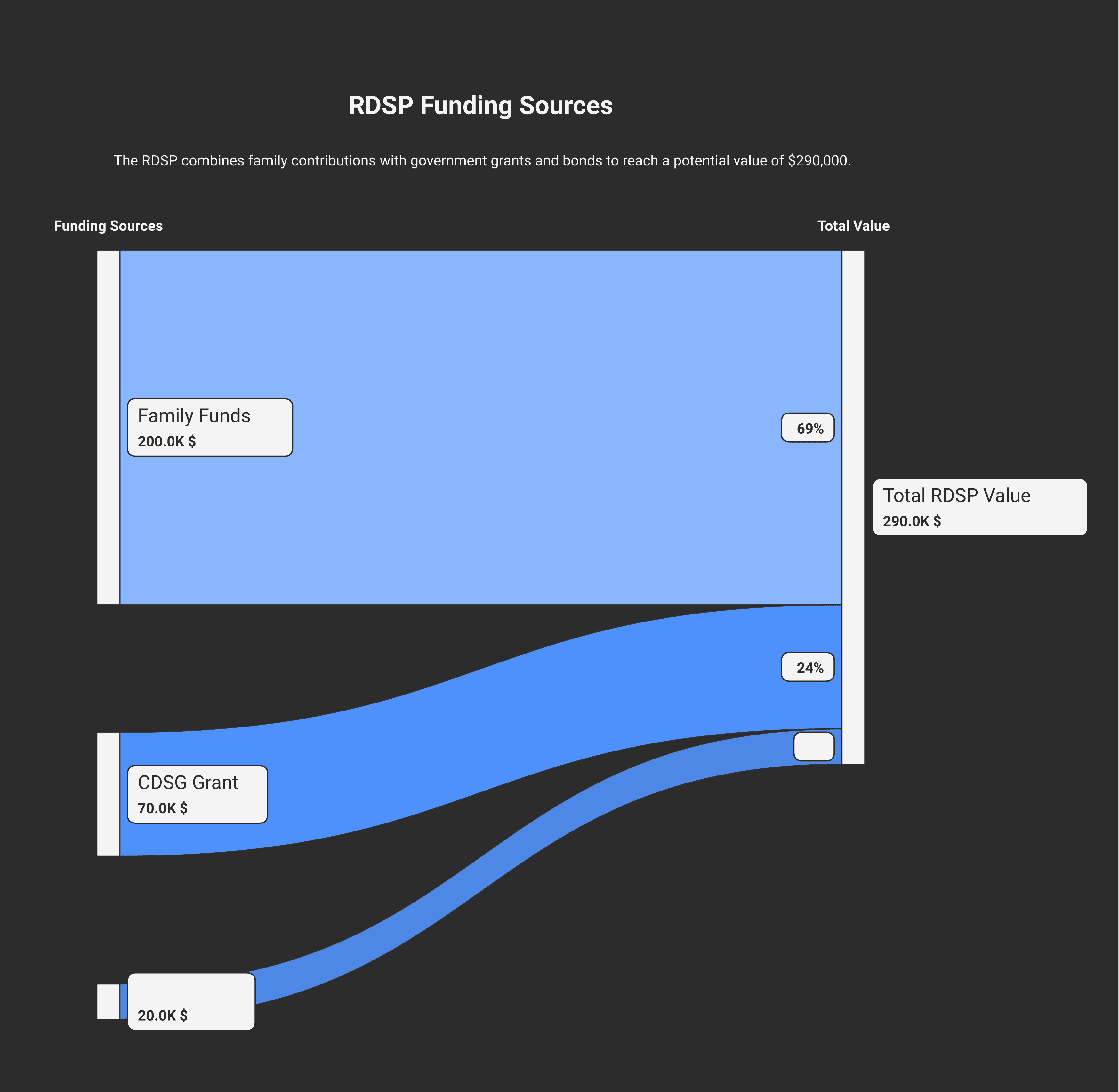

The Registered Disability Savings Plan is the most underused tax-advantaged account in Canada. A beneficiary who is eligible for the disability tax credit can have up to $90,000 of federal government money deposited into their RDSP over their lifetime — $70,000 of Canada Disability Savings Grants plus $20,000 of Canada Disability Savings Bonds — on top of family contributions that can reach $200,000.

Most CPAs come across families with an approved Form T2201 who never opened an RDSP. A 10-year-old child with DTC approval whose parents start the plan today with even modest contributions can pull more than $50,000 of grants forward by age 18 — without a single tax-planning move beyond opening the account and timing the deposit before December 31 each year.

This guide walks through how the RDSP works under section 146.4 of the Income Tax Act and the Canada Disability Savings Act, how the CDSG and CDSB stack, the carry-forward rule that lets you catch up on missed years, the 10-year assistance holdback that traps grants if you withdraw early, and the withdrawal mechanics through DAP and LDAP.

Key takeaways

The RDSP lifetime contribution cap is $200,000 per beneficiary under paragraph 146.4(4)(g)(iii) of the Income Tax Act. There is no annual contribution limit and contributions are not tax-deductible — the tax advantage is tax-deferred growth inside the plan plus the matched government deposits.

Two government programs deposit into the plan automatically when family income and contribution conditions are met: Canada Disability Savings Grants up to $70,000 lifetime ($3,500 max per year) and Canada Disability Savings Bonds up to $20,000 lifetime ($1,000 max per year).

For 2026, families with adjusted net income at or below $117,045 receive 3:1 matching on the first $500 of contributions and 2:1 on the next $1,000 — meaning a $1,500 contribution attracts $3,500 of grant. Above that threshold, matching drops to 1:1 on the first $1,000 contributed.

Grants and bonds are paid until the end of the calendar year the beneficiary turns 49. Carry-forward of unused grant and bond entitlement reaches back up to 10 prior years, but each year has its own annual maximum claim (currently $10,500 CDSG and $11,000 CDSB in any single year).

The Assistance Holdback Amount (AHA) under the Canada Disability Savings Regulations is the total CDSG and CDSB paid into the plan in the preceding 10 years, less any portion already repaid. Repayment is triggered by AHA events: plan closure, beneficiary death, plan non-compliance, withdrawals (DAP/LDAP), and — only when combined with closure — DTC ineligibility. The repayment formula differs by event type: closure/death/non-compliance trigger full AHA repayment, while a DAP/LDAP triggers proportional repayment ($3 of CDSG/CDSB per $1 withdrawn, capped at the AHA) under the rule in effect since January 1, 2014.

What an RDSP is — and what it isn't

The RDSP was introduced in 2008 under section 146.4 of the Income Tax Act. Mechanically it is a trust governed by an issuer (most major Canadian banks and a handful of credit unions and trust companies offer them) for the benefit of a single DTC-eligible beneficiary. There is one beneficiary per plan and one plan per beneficiary.

The plan has three sources of funding:

Family contributions — anyone the holder authorises can contribute on behalf of the beneficiary, up to a lifetime aggregate of $200,000. Contributions are not tax-deductible. There is no annual contribution limit beyond the lifetime cap.

Canada Disability Savings Grant (CDSG) — federal matching of family contributions, up to $3,500 per year and $70,000 lifetime, based on the beneficiary's adjusted family net income from two tax years prior.

Canada Disability Savings Bond (CDSB) — federal deposit for low-income beneficiaries, up to $1,000 per year and $20,000 lifetime, paid regardless of whether any contribution is made.

Income inside the plan — interest, dividends, capital gains — accumulates tax-free. Tax is only paid when the beneficiary receives a withdrawal, and even then only on the grant/bond/income portion, not the contribution portion.

What the RDSP is not:

It is not a retirement plan. Contributions stop at the end of the year the beneficiary turns 59. Grants and bonds stop at 49. There is no annual top-up after retirement age the way an RRSP allows.

It is not means-tested in the conventional sense, but the grant matching tier depends on family income (or, after age 18, the beneficiary's own income with spousal income combined).

It is not a creditor-proof trust in the typical sense — provincial law governs whether the plan is exempt from creditors in the beneficiary's province.

It is not portable across beneficiaries. The plan is tied to a specific beneficiary. Since Bill C-30 took effect on January 1, 2021, the plan may stay open indefinitely after the beneficiary loses DTC eligibility — contributions, grants, and bonds simply pause until eligibility is restored.

DTC eligibility is the gate

You cannot open an RDSP unless the beneficiary has an approved Form T2201, Disability Tax Credit Certificate on file with the CRA. Subsection 146.4(1)'s definition of "DTC-eligible individual" cross-references section 118.3 directly. We cover the application process and the eight eligibility categories in our disability tax credit guide.

Two important wrinkles on the DTC requirement:

Retroactive DTC approval unlocks retroactive grants and bonds. When CRA approves a Form T2201 retroactively for prior tax years, the beneficiary becomes eligible for CDSG and CDSB entitlement for those prior years. If the RDSP is opened and contributions made within the timing rules (see carry-forward below), those retroactive years can be claimed. For new immigrants to Canada with a child or adult dependant who has had a long-term impairment from before arrival, the retroactive window only runs from the year residency starts — earlier years cannot be claimed because the beneficiary was not a Canadian resident.

Loss of DTC eligibility — the rules changed in 2021. If the beneficiary's DTC approval is not renewed (CRA approvals usually run 5 or 10 years), the rules now allow the plan to stay open indefinitely. This is a meaningful improvement over the pre-2021 regime. The prior rules required the plan to be closed by the end of the year following the first full calendar year throughout which the beneficiary was no longer DTC-eligible, unless a specific election (the former "DTC Election" under subsection 146.4(4.1)) was filed. Bill C-30, effective January 1, 2021, removed both the closure requirement and the DTC Election itself. During a period of DTC ineligibility no new contributions, CDSG, or CDSB can be deposited, and the AHA window is modified for older beneficiaries — see the "Assistance holdback" section below.

CDSG — the matching grant

The Canada Disability Savings Grant is paid under the Canada Disability Savings Act administered by Employment and Social Development Canada. It matches family contributions at a tier rate based on the beneficiary's adjusted family net income from two tax years prior — so 2026 grant entitlement is based on 2024 family income.

For 2026 (ESDC Notice #577):

Adjusted family net income (2024) | Matching tiers | Maximum grant |

|---|---|---|

Up to $117,045 | 3:1 on first $500 contributed (→ $1,500), then 2:1 on next $1,000 (→ $2,000) | $3,500 per year |

Above $117,045 | 1:1 on first $1,000 contributed (→ $1,000) | $1,000 per year |

Lifetime CDSG cap: $70,000. Annual maximum (current-year only, regardless of income tier): $3,500. Grant entitlement is calculated separately for each calendar year; unused entitlement carries forward to future years, subject to an annual carry-forward draw cap of $10,500 (see below).

Two practical implications:

The $1,500 sweet spot. For families at or below the $117,045 threshold, $1,500 of contributions in a single year produces $3,500 of matching grant — a 2.33x return on the contribution before any plan growth. Contributing more than $1,500 in a year still helps the lifetime cap, but no additional matching is paid above $3,500 in any calendar year (subject to carry-forward, where applicable).

Family income determines tier, but the rolling two-year lag matters. A family whose 2024 income was below $117,045 receives the high-tier match in 2026, even if 2026 income has risen significantly. This timing creates planning opportunities for families with variable income.

CDSB — the no-contribution bond

The Canada Disability Savings Bond pays low-income beneficiaries up to $1,000 per year into the RDSP without any contribution being required. The plan only needs to be open. Lifetime cap: $20,000.

For 2026, based on 2024 adjusted family net income:

Adjusted family net income (2024) | CDSB amount |

|---|---|

At or below $38,237 | $1,000 (full bond) |

Between $38,237 and $58,523 | Phased — calculated proportionally |

Above $58,523 | $0 |

The CDSB is the cleanest case of "free money" the Canadian tax system offers. A low-income family that simply opens an RDSP and never contributes can still receive $20,000 of federal deposits over 20 years.

Carry-forward — up to 10 prior years

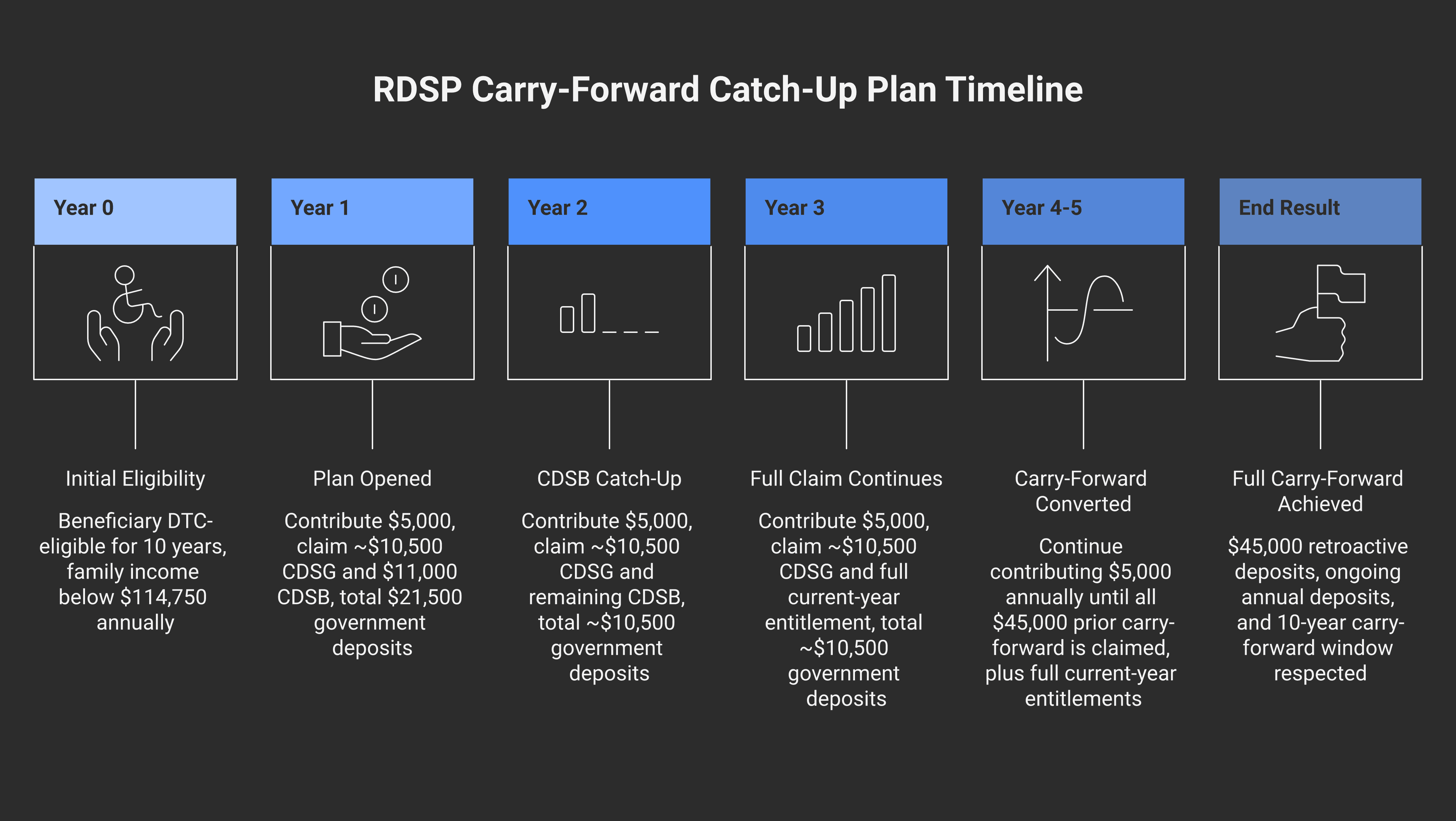

This is where the RDSP becomes interesting for late-starting families. Both the CDSG and CDSB allow carry-forward of unused entitlement for up to 10 prior years (back to 2008 when the program launched, whichever is later), subject to a few rules:

The beneficiary must have been DTC-eligible for each prior year being claimed. If DTC approval is retroactive, those prior years become claimable.

The beneficiary must have been resident in Canada for each year being claimed.

The annual maximum carry-forward draw is $10,500 of CDSG and $11,000 of CDSB in a single calendar year. So a family catching up 10 years of unused entitlement does it in chunks across multiple years, not in a single deposit.

Carry-forward is paid from oldest year to newest. So 2016 entitlement is paid before 2017, and so on.

This is the mechanic that drives the most consequential RDSP planning move: families who learn about the RDSP late should open it as soon as possible (even with no contribution, to start the CDSB clock), then ramp contributions over the next few years to convert as much carry-forward entitlement as possible before age 49.

A worked example of the principle: a beneficiary who has been DTC-eligible for the past 10 years but never had an RDSP, whose family income has been below $114,750 each of those years, has accumulated unused CDSG entitlement of $35,000 ($3,500 × 10) and CDSB entitlement of $10,000 ($1,000 × 10). With the right contribution sequence over the next four to five years, all of that entitlement can be pulled into the plan.

The assistance holdback amount (AHA) — how repayments actually work

The most important — and most misunderstood — rule in the RDSP system is the assistance holdback amount (AHA). It is defined in section 1 (Interpretation) of the Canada Disability Savings Regulations as the total of all CDSG and CDSB paid into the plan in the preceding 10 years, less any portion already repaid.

The AHA is what the issuer tracks continuously — a running 10-year sum of grants and bonds — and it is the minimum balance the plan must protect against premature withdrawal. But the repayment formula depends on which AHA event is triggered.

Two repayment formulas — not one

Full AHA repayment is triggered by:

Plan closure (voluntary termination)

Death of the beneficiary

Plan non-compliance (e.g., the plan no longer meets registration conditions)

Closure during a period of DTC ineligibility (post-2021)

In any of these events, the issuer repays to the Government of Canada the lesser of the plan's fair market value and the full AHA at the time of the event.

Proportional repayment (often called the "$3-for-$1 rule") is triggered by:

A Disability Assistance Payment (DAP) — a one-time withdrawal

A Lifetime Disability Assistance Payment (LDAP) — the annual periodic stream

Since January 1, 2014, when a DAP or LDAP is made, the issuer must repay to the Government of Canada the lesser of:

$3 of CDSG and CDSB for every $1 of disability assistance payment made, and

The current AHA.

So a $5,000 DAP from a plan with an AHA of $30,000 triggers a repayment of $15,000 of grants and bonds — not the full $30,000. The plan delivers $5,000 to the beneficiary and remits $15,000 to the government; the AHA shrinks by $15,000.

This proportional rule is the single most important detail in RDSP withdrawal planning. The pre-2014 rule (full AHA recovery on any DAP) created a steep all-or-nothing penalty; the post-2014 proportional rule lets families make modest mid-life withdrawals when needed, with predictable cost.

What about loss of DTC eligibility?

DTC ineligibility on its own is no longer an AHA repayment trigger. Per the rules in force since January 1, 2021 (Bill C-30):

A plan may continue indefinitely after the beneficiary loses DTC eligibility.

Contributions, CDSG, and CDSB pause during ineligibility.

The AHA only becomes repayable if the plan is closed during a period of DTC ineligibility — at which point full AHA repayment applies.

Per ESDC InfoCapsule 17: an AHA event can be a withdrawal (DAP or LDAP), the death of the beneficiary, plan closure, plan non-compliance, or closure during DTC ineligibility. DTC loss without closure does not trigger repayment.

The age-50+ AHA reduction

A second piece of the modernised AHA rules: for plans in a period of DTC ineligibility, the AHA's 10-year lookback shrinks as the beneficiary ages, ultimately reaching zero. Specifically:

For each year the beneficiary's age (at year-end of the AHA event) exceeds 50, the AHA period reduces by one year.

By the year the beneficiary turns 60, the AHA period is nil — meaning no AHA repayment is owing for any AHA event in that or subsequent years during DTC ineligibility.

This is the underlying mechanic for the "exit the holdback by age 60" planning point that has long applied to RDSPs, now formalised in the regulations after Bill C-30.

Specified Disability Savings Plan (SDSP) — a separate carve-out

Distinct from the AHA reduction above, an RDSP can be converted to a Specified Disability Savings Plan (SDSP) when a medical practitioner certifies that the beneficiary is unlikely to live more than five years. Once the SDSP election is filed, the plan can pay withdrawals where the taxable portion of those withdrawals does not exceed $10,000 per year (or, if larger, the year's LDAP formula amount) without triggering AHA repayment. The trade-off: no new contributions can be made, and no new CDSG or CDSB will be paid into an SDSP.

Practical consequences

Plan opened young, withdrawn after age 60, grants and bonds keep flowing. For a child beneficiary, contributions made in early years build a plan whose AHA shrinks toward zero by the time the beneficiary is in their early 60s. The age-50+ reduction reinforces the "open early, hold long" planning principle.

Late-starting families can still make modest withdrawals without losing everything. The proportional rule means a $1,000 DAP costs $3,000 of grants and bonds — not the entire AHA. Withdrawal planning becomes about pacing, not avoidance.

DTC denial after years of grants is no longer the catastrophe it once was. The plan can stay open indefinitely during DTC ineligibility, and AHA repayment is only triggered if the plan is closed during that ineligibility period.

Withdrawals — DAP and LDAP

Two types of withdrawals are possible from an RDSP under section 146.4:

Disability Assistance Payment (DAP). A one-time (or occasional) payment from the plan to the beneficiary. DAPs trigger the proportional AHA repayment: $3 of CDSG/CDSB per $1 withdrawn, capped at the current AHA — see the AHA section above.

Lifetime Disability Assistance Payment (LDAP). Annual payments that, once started, must continue at least annually until the beneficiary's death or plan termination. LDAP payments must begin no later than the end of the year the beneficiary turns 60. LDAP payments are also subject to the proportional AHA repayment rule (same $3:$1 formula).

LDAP amounts are calculated under a statutory formula in subsection 146.4(1):

Maximum LDAP = A / (B + 3 - C) + D

Where:

A = fair market value of plan assets at the start of the year

B = greater of 80 or the beneficiary's age at the start of the year

C = beneficiary's age at the start of the year

D = any periodic annuity payments received by the plan that year

The formula is designed to spread the plan's assets across the beneficiary's expected lifetime, with the denominator (B + 3 - C) representing remaining years. The formula does not produce maximum-out-the-account payments — it is conservative by design, and the beneficiary's actual LDAP can be larger only in specific circumstances (e.g., the plan's annual maximum LDAP is also subject to a minimum equal to the annual minimum withdrawal under the LDAP table). The minimum LDAP after age 60 is set by issuer-specific actuarial tables that approximate the RRIF-equivalent minimum.

Tax treatment of DAP/LDAP withdrawals. Every withdrawal is split proportionally between:

The contribution portion (return of capital, tax-free), and

The grant/bond/income portion (taxable to the beneficiary as ordinary income)

The proportions are set by the plan's running balance of contributions versus grants/bonds/income. For most plans where the government deposits and accumulated investment income are significant relative to contributions, the majority of each withdrawal is taxable. For most RDSP beneficiaries, ordinary tax rates on the withdrawal are well below the cost of foregoing the grants and bonds in the first place — the math comes out strongly in favour of contributing.

Planning moves CPAs make

A few practical moves for families considering an RDSP, in rough priority order:

Open the plan the year DTC approval lands. Even with a zero contribution, opening the plan starts the CDSB clock for low-income families and locks in the CDSG carry-forward right. We routinely see families who waited a year or two after DTC approval before opening the plan and lost that year's CDSB entirely.

Target the $1,500 sweet spot annually if family income allows. For families at or below the $114,750 threshold, $1,500 of contributions a year converts the maximum CDSG of $3,500 — a 2.33x return on the contribution. Above $1,500, additional contributions still build the plan's principal but draw no matching beyond that year's $3,500 cap.

Re-examine carry-forward after retroactive DTC approval. When a Form T2201 is approved retroactively, file a T1-ADJ for each prior year to confirm DTC status, then open the RDSP and begin claiming carry-forward CDSG/CDSB.

Coordinate with provincial disability benefits. Provincial assistance programs (BC Disability Assistance, ODSP in Ontario, AISH in Alberta) treat RDSP differently. In most provinces, RDSP assets and income are exempt from provincial disability assistance income/asset tests — but the rules vary, and re-verifying before transferring assets into the plan matters.

Coordinate the RDSP with a Henson or discretionary trust where one exists. For families with substantial assets earmarked for a beneficiary with a long-term disability, the RDSP is one piece of a larger plan that often includes a family trust and may interact with the income-splitting toolkit on the supporting-parent side. The plans are complementary, not substitutes — the RDSP delivers government matching that no trust can replicate, and the trust delivers control and creditor protection the RDSP cannot.

Build the holdback runway into the family financial plan. A 5-year-old child with newly approved DTC and an RDSP opened today has 44 years before age 49 (the last year of grant/bond entitlement) and effectively a clear withdrawal runway starting around age 59. Families with adult beneficiaries face a tighter window.

For most families with a child or adult dependant with a long-term disability, the RDSP combined with the disability tax credit stack is the single most consequential piece of long-term tax planning. At Modern Axis, we frequently coordinate RDSP timing with DTC application, retroactive T1 adjustments, and the broader family tax planning picture — including salary-versus-dividend decisions for the supporting parent's marginal-rate management. If you have a beneficiary in the family but no plan open, the highest-leverage move is usually to open it before December 31 of this year.

Frequently asked questions

How much can the government deposit into an RDSP?

Up to $90,000 over the beneficiary's lifetime: $70,000 from the Canada Disability Savings Grant (matching family contributions, capped at $3,500 per year) and $20,000 from the Canada Disability Savings Bond (paid to low-income beneficiaries without any contribution required, capped at $1,000 per year). Both programs are paid until the end of the calendar year the beneficiary turns 49, under the Canada Disability Savings Act administered alongside section 146.4 of the Income Tax Act.

What is the 10-year holdback rule on RDSP grants?

The "assistance holdback amount" (AHA) is the total CDSG and CDSB paid into the plan in the preceding 10 years, less any portion already repaid, defined in section 1 (Interpretation) of the Canada Disability Savings Regulations. Repayment is triggered by AHA events. For plan closure, beneficiary death, plan non-compliance, or closure during a period of DTC ineligibility, the full AHA is repayable. For a Disability Assistance Payment (DAP) or Lifetime Disability Assistance Payment (LDAP), since January 1, 2014 the proportional rule applies — $3 of CDSG/CDSB must be repaid to the federal government for every $1 withdrawn, capped at the AHA. The AHA's 10-year lookback shrinks one year per year of beneficiary age above 50, reaching zero at age 60.

Do I need to contribute to an RDSP to receive the Canada Disability Savings Bond?

No. The Canada Disability Savings Bond is paid automatically to plans whose beneficiary's family income is below the threshold ($38,237 for 2026 full bond; phased between $38,237 and $58,523). Opening the plan is the only requirement — no contribution is needed. Bonds are paid until the end of the year the beneficiary turns 49.

Who can be a holder of an RDSP for an adult beneficiary?

If the beneficiary is over 18 and capable of managing their own affairs, they are the holder. If the beneficiary is over 18 and not capable of managing their financial affairs, a qualifying family member (parent, spouse, or common-law partner) can act as holder under a federal temporary measure that has been extended through 2026, or a court-appointed guardian/trustee acts as holder under provincial law. The rules differ by province.

Can I carry forward unused CDSG entitlement?

Yes. Unused CDSG and CDSB entitlement carries forward for up to 10 prior years, subject to annual maximum claims of $10,500 CDSG and $11,000 CDSB in a single year. Carry-forward is paid from oldest year to newest. The beneficiary must have been DTC-eligible and resident in Canada for each prior year being claimed.

How are RDSP withdrawals taxed?

Withdrawals (Disability Assistance Payments or Lifetime Disability Assistance Payments) are split proportionally between the contribution portion (tax-free return of capital) and the grant/bond/investment-income portion (taxable to the beneficiary as ordinary income). The proportions are set by the plan's running balance of contributions versus other deposits. Most RDSP withdrawals are majority-taxable because grants, bonds, and accumulated growth typically exceed family contributions over time.

What happens to the RDSP if the beneficiary loses DTC eligibility?

Since Bill C-30 took effect on January 1, 2021, the plan can stay open indefinitely if the beneficiary loses DTC eligibility. No new contributions, CDSG, or CDSB can be deposited during a period of DTC ineligibility, but the plan continues to grow tax-deferred. The former "DTC Election" under subsection 146.4(4.1) was eliminated by Bill C-30. AHA repayment is only triggered if the plan is closed during a period of DTC ineligibility — and the AHA's 10-year lookback shrinks one year per year of beneficiary age above 50, reaching zero at age 60.

A note before you go: this post covers general principles, not your specific situation. Tax and benefit outcomes turn on facts — residency, family income, DTC status, timing — and an article can't capture all of that. Treat this as a starting point rather than advice to rely on, and talk to a CPA or tax lawyer about your own circumstances before making any decisions based on what you've read.

Alex Ataman, CPA

Founder

Modern Axis CPA