Tax Considerations for Immigrants

Canada’s Taxation of Worldwide Income

Canada’s tax system operates on a worldwide income basis, meaning that once you become a tax resident, you must report all income earned globally, regardless of whether the money is brought into Canada. This includes interest earned from foreign bank accounts, rental income from properties owned outside Canada, pensions received from foreign sources, and capital gains from selling inherited or other foreign property. For example, if you inherited a property abroad before immigrating and later sell it as a Canadian resident, you could be subject to capital gains tax on the increase in value from the fair market value (FMV) at the time of your arrival to the sale price. Similarly, if you owned foreign investments or shares that appreciated in value after your immigration, any gains upon sale would also be taxable in Canada.

Key takeaways

Canada taxes new immigrants on worldwide income from the date they become tax residents under ITA section 250, not from the date they enter the country, so first-year filing requires careful date allocation.

All assets owned at the moment of immigration receive a deemed acquisition at fair market value under ITA section 128.1(1)(c) — capturing this FMV in writing on arrival is the single most important first-year compliance task.

Foreign property over $100,000 in cost amount triggers annual T1135 Foreign Income Verification reporting; non-disclosure penalties under ITA section 162(7) start at $2,500 and rise to $24,000 plus 5 percent of the asset cost.

Foreign corporations controlled by the immigrant trigger T1134 reporting and potential Foreign Accrual Property Income (FAPI) attribution under ITA subsections 91 to 95, regardless of whether any cash is repatriated to Canada.

Failing to report foreign income can result in severe penalties and interest charges, making it critical for newcomers to understand and comply with their tax obligations.

Fair Market Value (FMV) of Assets Upon Arrival

When immigrating to Canada, all assets owned before arrival must be valued at fair market value (FMV) on the date of entry. The FMV of these assets is deemed to be their cost base for tax purposes and will impact future capital gains calculations when these assets are sold.

Proper Documentation of FMV

The CRA requires that FMV assessments be conducted by professionals, such as:

Real Estate Agents or Valuators: For properties owned outside Canada.

Certified Appraisers: For high-value assets like artwork, jewelry, and collectibles.

Business Valuators: For shares in foreign corporations.

Financial Statements & Market Data: For investment portfolios, stocks, and bonds.

Proper documentation ensures accurate reporting and reduces the risk of tax disputes with the CRA.

Optional 45(2) Election for Foreign Real Estate

If you own a property in your home country and decide to rent it out upon moving to Canada but plan to sell it before purchasing a home in Canada, you may be able to avoid capital gains tax by making an election under subsection 45(2) of the Income Tax Act. This election allows you to treat your foreign property as your principal residence for up to four years, even if it is rented out, provided you do not claim another principal residence in Canada during that period.

Key Considerations for the 45(2) Election:

The election must be filed with your tax return for the year the property starts being rented.

If the property is sold before purchasing a home in Canada, it may reduce or eliminate capital gains tax.

If you do not make this election, the property may be subject to capital gains tax from the date of your immigration to Canada.

This election can be beneficial for newcomers who are transitioning their financial affairs and planning to purchase property in Canada in the near future.

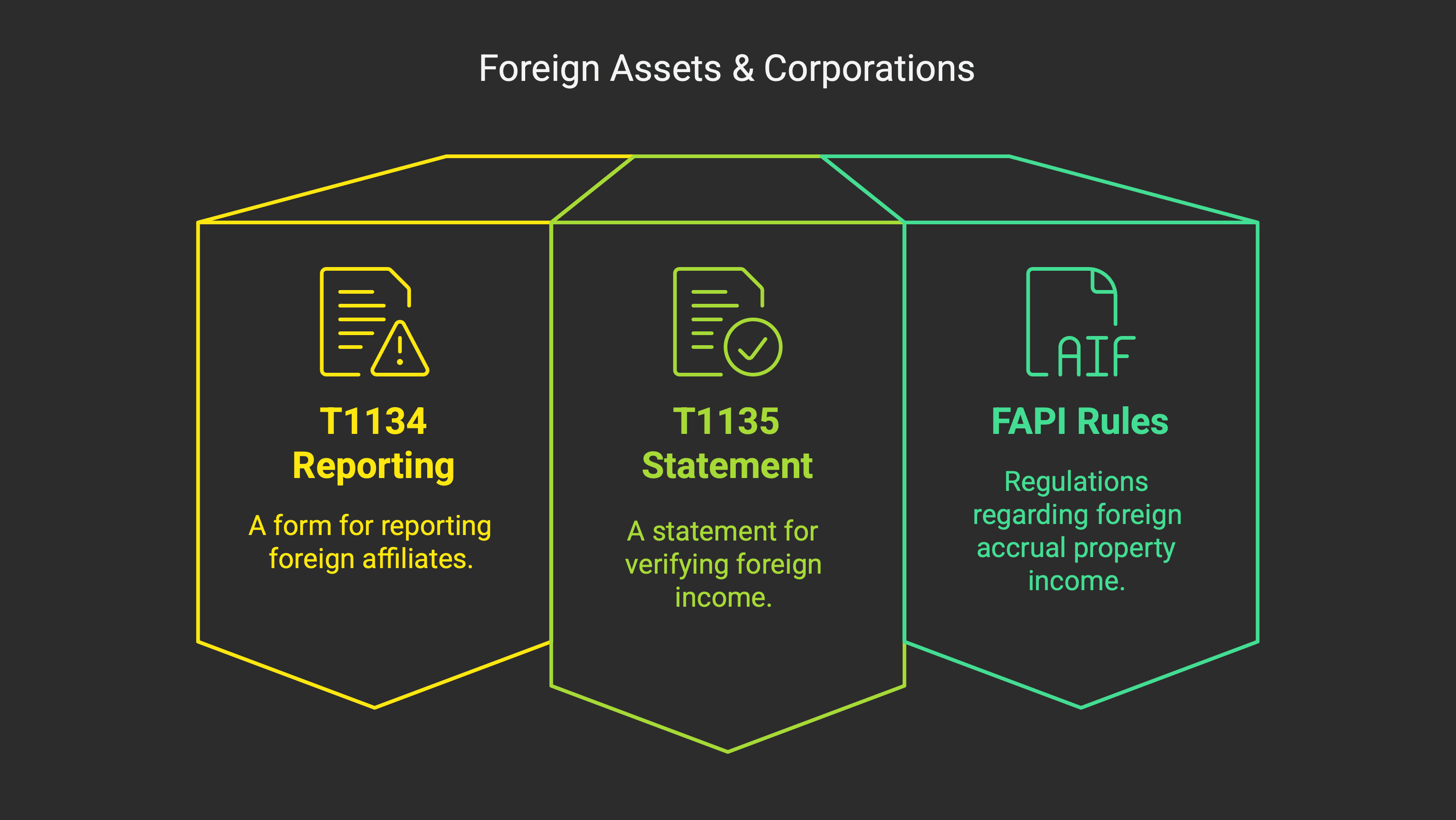

Compliance Requirements for Foreign Assets & Corporations

Newcomers who own foreign assets or interests in corporations must comply with additional tax reporting requirements.

1. T1134 – Foreign Affiliate Reporting

If you own at least 10% of a foreign corporation, either directly or indirectly, you may need to file Form T1134 (Information Return Relating to Controlled and Non-Controlled Foreign Affiliates). This form provides details about:

The foreign corporation’s financial information.

The nature of your investment.

Any income earned and repatriated to Canada.

Failure to file T1134 can result in penalties, even if no taxes are owed.

2. T1135 – Foreign Income Verification Statement

If your foreign assets exceed $100,000 CAD (excluding personal-use property like a vacation home), you must file Form T1135. This includes:

Foreign bank accounts.

Investments in foreign stocks (held outside Canadian brokerage accounts).

Interests in foreign businesses.

Rental properties outside Canada.

Penalties for failing to file T1135 are significant, with fines accruing daily for non-compliance.

3. Foreign Accrual Property Income (FAPI) Rules

If you control a foreign corporation, you may be subject to FAPI rules. These rules are designed to prevent Canadian taxpayers from deferring tax on passive income earned in foreign entities. The key implications include:

Passive income (e.g., interest, dividends, rental income) from the controlled foreign corporation is taxable in Canada, even if it is not distributed.

You must report this income annually and pay tax on it as if it were earned personally.

Why Proper First-Year Tax Filing Matters

Filing your first Canadian tax return accurately is essential to avoid penalties and ensure compliance with Canadian tax laws. Proper FMV documentation and disclosure of foreign assets and income prevent costly audits and financial consequences.

If you’re a newcomer with foreign assets or business interests, ModernAxis can help navigate these complex tax requirements and ensure full compliance with CRA regulations.

Disclaimer: This blog post is for informational purposes only and does not constitute professional tax advice.

Frequently asked questions

When do I become a tax resident of Canada as a new immigrant?

You become a Canadian tax resident on the date you establish significant residential ties — typically the date you arrive with the intent to settle, secure permanent housing, and bring family. CRA applies a facts-and-circumstances residential-ties test set out in Income Tax Folio S5-F1-C1. Your first Canadian return covers worldwide income from that residency date forward, while income earned before arrival is reported only if it would otherwise be Canadian-source.

Do I have to pay Canadian tax on income earned before I immigrated?

Generally no, unless it was Canadian-source income (such as rental from a Canadian property or employment performed in Canada). Pre-residency foreign employment income, foreign rental income, and foreign investment income are not taxed in Canada. The split happens on your "date of arrival," and your first Canadian return prorates personal credits and basic personal amount accordingly.

What is fair market value of assets at immigration and why does it matter?

Under ITA section 128.1(1)(c), Canada treats you as having acquired all your assets at FMV on the date you became a tax resident. This "stepped-up basis" means future capital gains are measured from the FMV at immigration, not from your original purchase price. Documenting FMV in writing (appraisals, brokerage statements, comparable sales) on the arrival date is critical — without it, CRA may default to original cost and over-tax future gains.

Do I need to report foreign property on my Canadian tax return?

Yes, if the total cost amount of specified foreign property exceeds $100,000 CAD at any point in the year. Form T1135 captures foreign bank accounts, investment accounts, real estate (other than personal-use), and foreign corporate shares. The reporting threshold is cost amount, not market value, and applies starting in your second year of Canadian residency. Penalties under ITA section 162(7) for non-filing start at $2,500.

What is a T1134 and when does it apply to new immigrants?

Form T1134 is the Information Return Relating to Controlled and Non-Controlled Foreign Affiliates. Any Canadian resident who owns at least 10 percent of a foreign corporation directly or indirectly, or who is one of multiple Canadians collectively owning more than 50 percent, must file annually. Penalties start at $2,500 per affiliate. Foreign Accrual Property Income (FAPI) rules under ITA sections 91 to 95 can attribute passive income of the foreign corporation back to you personally even with no dividend paid.

Can I keep my foreign rental property without triggering Canadian tax?

No — once you are a Canadian tax resident, rental income from foreign real estate is fully taxable in Canada under the worldwide income principle. You may elect under ITA section 45(2) to defer the deemed disposition rules on a former principal residence converted to rental, which preserves the principal residence exemption for up to four years. Foreign tax paid generates a foreign tax credit, but careful coordination is needed to avoid double taxation.

Alex Ataman, CPA

Founder

Modern Axis CPA