Disability Tax Credit Canada: Complete Guide

The disability tax credit is the most consequential tax credit most eligible Canadians never claim. It is worth around $1,500 in federal tax savings per year on its own — but the real value sits behind it. Without an approved Form T2201 on file with the CRA, you cannot open a Registered Disability Savings Plan, claim the Canada Disability Benefit, claim the Canada Caregiver Credit on a dependant, or get the Home Accessibility Tax Credit at full strength. Approval unlocks a stack of other programs that, over a working lifetime, can be worth six figures.

So when a CPA says "let's get this filed," it is not really about the line 31600 deduction. It is about the door the certificate opens. And the door is closed for tens of thousands of eligible Canadians because the application gets denied — almost always for reasons that come back to how the medical practitioner filled out the form, not whether the person actually qualifies.

This guide walks through what the disability tax credit is, what it unlocks, who qualifies under each of the eight categories of basic activities of daily living, how to apply, how to claim it retroactively for up to 10 prior tax years, and the specific reasons applications get rejected.

Key takeaways

The federal disability tax credit for 2026 is $10,341 multiplied by the 14% lowest federal rate — about $1,448 in federal tax reduction — under subsection 118.3(1) of the Income Tax Act. Most provinces add their own parallel credit. (Note: the federal lowest rate dropped from 15% to 14% effective July 1, 2025, applying for the full 2026 tax year. A separate "Top-Up Tax Credit" introduced in Budget 2025 preserves the 15% rate on aggregate non-refundable amounts in excess of the first bracket threshold for 2025–2030.)

Children under 18 get an additional federal supplement of $6,032 (about $844 of additional federal tax reduction), reduced dollar-for-dollar by attendant care or child care claims exceeding $3,533 for 2026.

Approval is the gate to the RDSP, the Canada Disability Benefit, the Child Disability Benefit, the Home Accessibility Tax Credit at the higher dependant rate, the Canada Caregiver Credit on a dependant, and the disability supports deduction.

Approval is retroactive. If the medical practitioner certifies the impairment as having existed in earlier years, the CRA will apply the credit (and unlock the RDSP and CDB retroactively) for up to 10 prior tax years through Form T1-ADJ.

Most denials are not about the impairment — they are about the wording on Form T2201. CRA does not review the patient's chart; it reviews what the practitioner wrote in the prescribed form.

What the disability tax credit actually is

The disability tax credit is a non-refundable federal tax credit created by section 118.3 of the Income Tax Act. For the 2026 tax year, the base disability amount is $10,341. Multiplied by the 14% lowest federal rate — reduced from 15% effective July 1, 2025 — that produces a federal tax reduction of about $1,448.

Every province except Quebec layers its own disability amount on top of the federal credit at the provincial low-rate, adding roughly another $500 to $900 of provincial tax reduction depending on where you live. In British Columbia, for example, the combined federal-plus-provincial value lands at roughly $2,000 per year.

A few important mechanical points:

Non-refundable means the credit can reduce your tax to zero but cannot generate a refund beyond what you actually paid in tax. If the person with the disability has no income, the credit transfers to a supporting spouse or other supporting person under subsection 118.3(2).

The credit is annual. It applies for every tax year the impairment exists. Once approved, you do not re-apply each year — the CRA's Disability Tax Credit Determination is good for a fixed period (often 5 to 10 years) and may be re-certified after that.

Supplement for children under 18. Children under 18 at year-end get an additional federal disability amount of $6,032 for 2026 — but it is reduced by attendant care or child care expenses claimed for that child that exceed $3,533. The supplement targets families paying out-of-pocket for specialised support rather than already deducting those costs elsewhere.

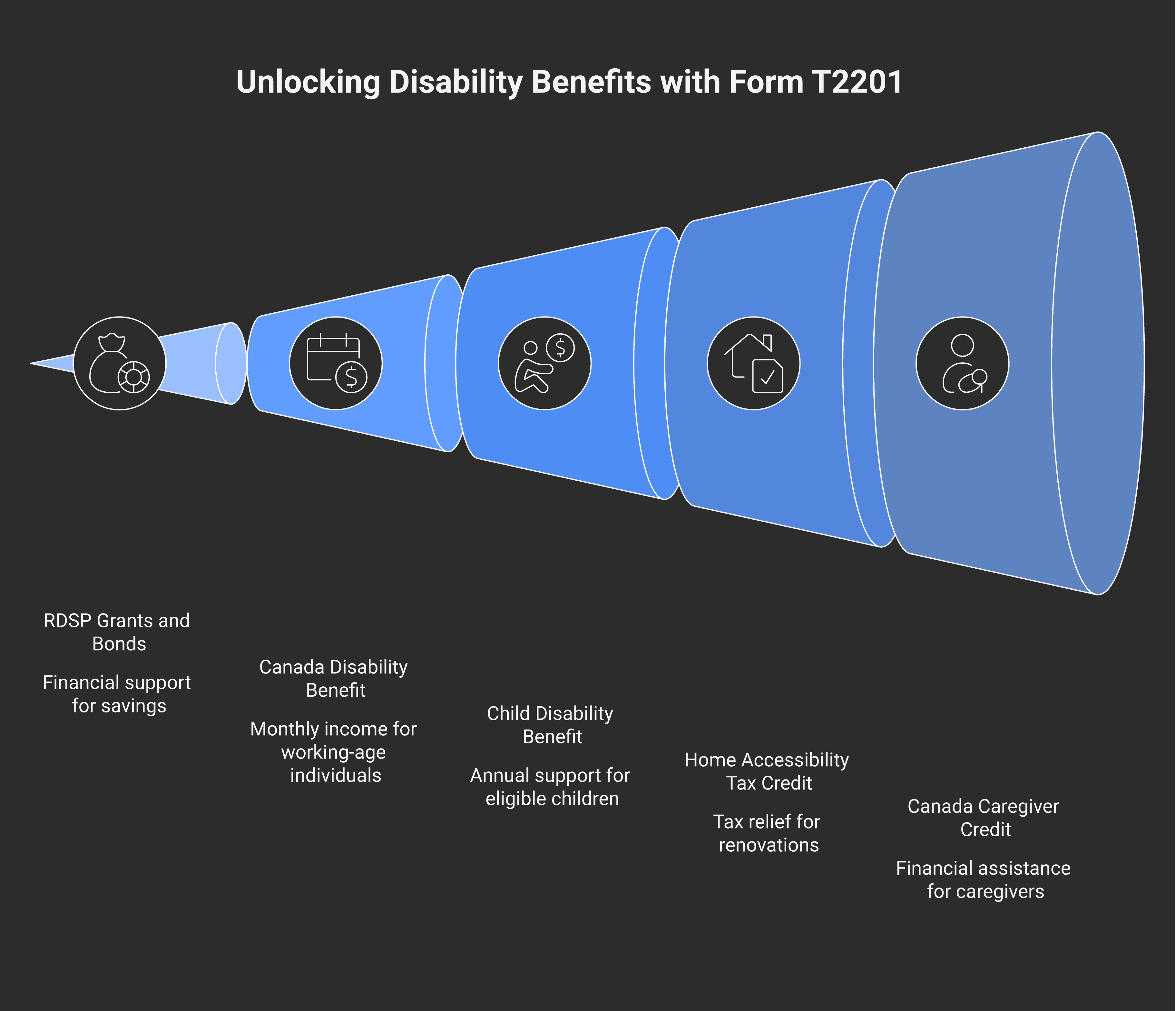

What approval unlocks (this is the real value)

The federal credit itself is meaningful, but every CPA who works with families with a child or adult dependant with a disability knows the bigger number sits in the programs that require an approved T2201 to access. Five of these are particularly valuable:

Registered Disability Savings Plan (RDSP). The RDSP is the most underused tax-advantaged account in Canada. Eligible beneficiaries can receive up to $70,000 of Canada Disability Savings Grants and up to $20,000 of Canada Disability Savings Bonds from the federal government over their lifetime — $90,000 of free money, on top of family contributions of up to $200,000. The RDSP only opens if the beneficiary has DTC approval on file. We cover the mechanics in our RDSP guide.

Canada Disability Benefit (CDB). Launched in 2025 under the Canada Disability Benefit Act, the CDB pays eligible working-age Canadians (18–64) up to $200 per month, indexed to inflation. DTC approval is a hard prerequisite for application. Without an approved T2201, the CDB application cannot proceed.

Child Disability Benefit. A monthly top-up to the Canada Child Benefit for families with a child under 18 who has DTC approval. For 2026, the maximum is approximately $3,411 per year per eligible child. This is delivered automatically to CCB-recipient families once the T2201 is approved — no separate application needed.

Home Accessibility Tax Credit (HATC). Allows up to $20,000 of eligible home renovation expenses per year to be claimed for a senior or a person with DTC approval. The 14% federal credit caps at $2,800 per year for 2026. The renovations must enable the person to be more functional or mobile within the home — ramps, widened doorways, walk-in tubs, grab bars.

Canada Caregiver Credit on a dependant. A supporting person caring for a spouse, eligible dependant, or other family member with a marked impairment can claim a federal Canada Caregiver Credit. For 2026 the base amount under line 30450 (for other infirm dependants 18 or older) is $8,773, producing approximately $1,228 of federal tax reduction at the 14% rate; the line 30500 amount for infirm children under 18 is $2,740 (~$384 federal). The amount is reduced by the dependant's net income above the indexed threshold. DTC approval substantiates the impairment and removes most of the documentation friction.

There are smaller benefits too — the Disability Supports Deduction, the medical expense tax credit baseline for attendant care, the GST/HST rebate at certain thresholds for transit-dependent individuals — but the five above account for most of the dollar value behind DTC approval.

Who qualifies: the eight categories

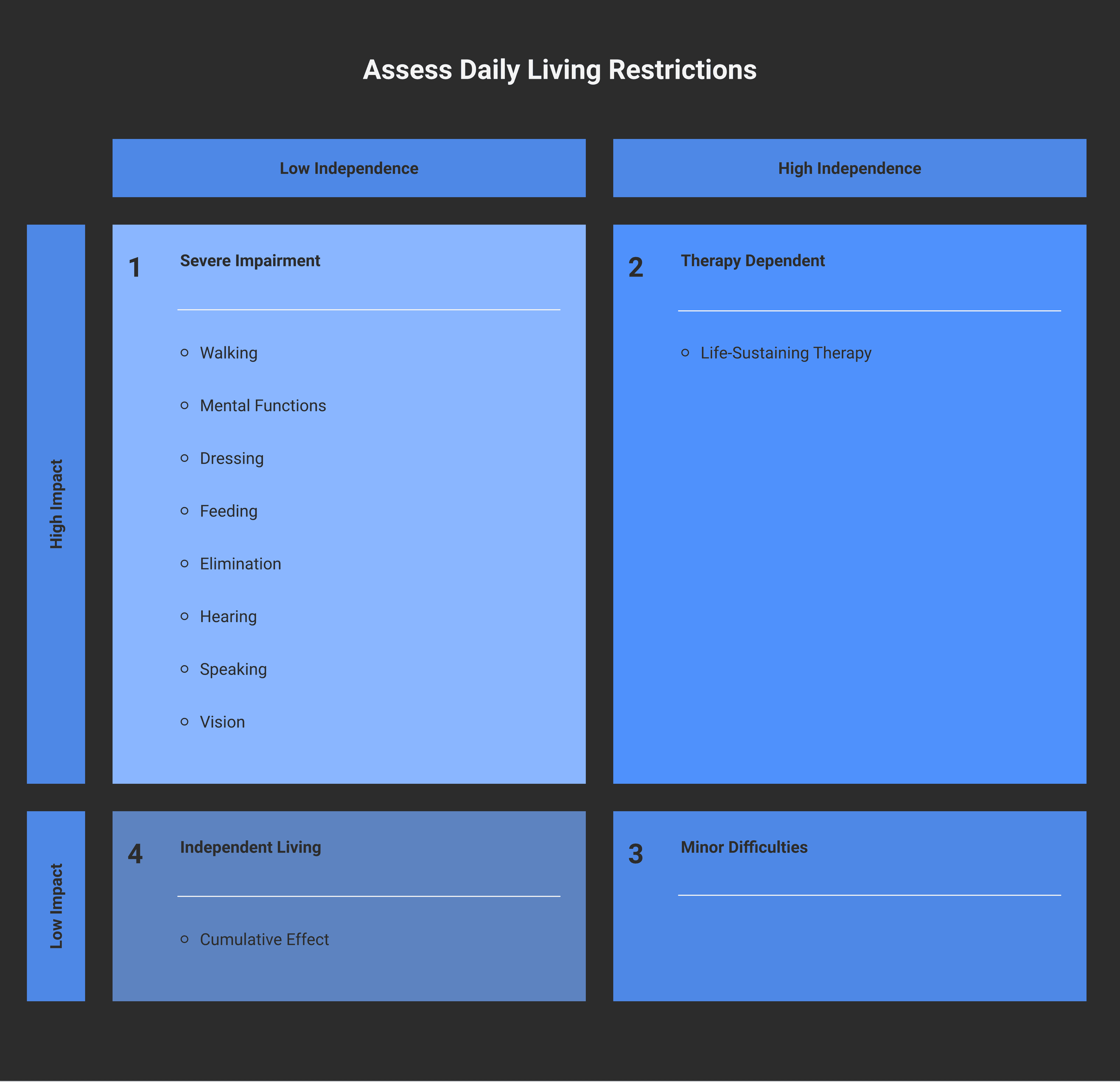

Subsection 118.3(1) of the Income Tax Act requires that an individual have one or more severe and prolonged impairments in physical or mental functions, and that the impairment produce one of the following: a marked restriction in a basic activity of daily living, a marked restriction in vision, the equivalent of a marked restriction through cumulative effect of significant restrictions in two or more activities, or the need for life-sustaining therapy of at least 14 hours per week.

Two definitions sit underneath:

Severe and prolonged means the impairment has lasted or is expected to last for a continuous period of at least 12 months.

Marked restriction means the person is unable, or takes an inordinate amount of time (CRA's working interpretation is at least three times as long as someone without the impairment), to perform a basic activity of daily living — even with appropriate therapy, medication, and devices — for all or substantially all of the time (typically 90% or more).

The eight categories the legislation and CRA Form T2201 walk through:

1. Walking. Markedly restricted ability to walk. Includes individuals who cannot walk 100 metres on level ground, or who require an inordinate amount of time to do so, even with mobility aids.

2. Mental functions necessary for everyday life. Includes memory, problem-solving, goal-setting, judgment, adaptive functioning (planning, organising, completing daily tasks), attention, and verbal/non-verbal comprehension. This is the category that has expanded the most over the last decade — covers conditions like autism spectrum disorders, severe ADHD, learning disabilities, traumatic brain injury, dementia, schizophrenia, bipolar disorder, severe depression, and developmental disabilities.

3. Dressing. Markedly restricted ability to dress, even with the use of devices and adapted clothing.

4. Feeding. Markedly restricted ability to feed oneself — preparing, identifying, selecting food and getting it into the mouth. Strict diets driven by chronic conditions (Crohn's, ulcerative colitis, severe food allergies, dysphagia) can qualify under feeding when they create an inordinate-time impairment.

5. Elimination. Markedly restricted ability to manage bowel or bladder function. Includes individuals managing severe inflammatory bowel disease, ostomy care that takes inordinate time daily, or post-treatment incontinence.

6. Hearing. Markedly restricted ability to hear, even with the use of appropriate devices. The CRA's standard is the inability to understand another person in a quiet setting using a hearing aid.

7. Speaking. Markedly restricted ability to speak so as to be understood, even with therapy, devices, and medication. Includes severe aphasia, post-stroke speech impairments, severe stammering, and certain neurodegenerative conditions.

8. Vision. Markedly restricted vision — defined as visual acuity of 20/200 or worse in both eyes with best correction, or a visual field of 20 degrees or less.

Beyond those eight, two alternative paths exist:

Cumulative effect of significant restrictions. If no single activity is markedly restricted, but two or more are significantly restricted (a lesser standard — typically inordinate-time at a lower threshold than marked, or marked for less than 90% of the time), and their cumulative effect is equivalent to being markedly restricted in one activity, the individual qualifies under paragraph 118.3(1)(a.2). This is the path that often wins for complex multi-system conditions — fibromyalgia, severe ME/CFS, long COVID, multiple sclerosis at certain stages — where no one activity hits the marked threshold but the combined burden does.

Life-sustaining therapy. Under subsection 118.3(1)(a.1)(ii), if without the therapy the individual would be markedly restricted, and the therapy must be administered at least two times each week for a total averaging at least 14 hours per week, the individual qualifies. After the 2022 amendment that added subsection 118.3(1.2), individuals with Type 1 diabetes are deemed to meet the 14-hour threshold automatically. This was a major win for the Type 1 community — before 2022, families had to log hours and document each step of insulin administration to qualify.

Form T2201 — what actually happens

The application is Form T2201, Disability Tax Credit Certificate. Two parts:

Part A is completed by the applicant (or the parent/legal representative). It identifies the person with the impairment, the supporting person who will claim the credit if the impaired person has no income, and authorises CRA to release decisions. Part A is administrative — there is no judgement here.

Part B is completed by a medical practitioner. This is the entire ballgame. CRA does not review the patient's chart, does not contact the family doctor for further detail, does not interview the patient. The CRA assessor reads what the practitioner wrote in Part B, then approves or denies.

Practitioners authorised to certify each section are specified in subsections 118.3(1)(a.2) and (a.3):

Category | Authorised practitioner |

|---|---|

Vision | Medical doctor, nurse practitioner, optometrist |

Speaking | Medical doctor, nurse practitioner, speech-language pathologist |

Hearing | Medical doctor, nurse practitioner, audiologist |

Walking, feeding, dressing | Medical doctor, nurse practitioner, occupational therapist; physiotherapist (walking only, since Feb 2005) |

Elimination | Medical doctor, nurse practitioner |

Mental functions | Medical doctor, nurse practitioner, psychologist |

Life-sustaining therapy | Medical doctor, nurse practitioner |

A useful tactic if you have access to multiple practitioners: the person who knows the impairment in clinical detail should complete that section. A family doctor who has seen the patient three times in two years will write a thinner Part B than an occupational therapist who has done a full functional assessment. CRA reads the detail.

After Part B, the form is submitted to the CRA (digital submission is now available through the patient's CRA My Account or by mail). The CRA's Disability Tax Credit Unit reviews and issues a Notice of Determination — typically within 8 to 12 weeks under normal volumes, longer during peak season.

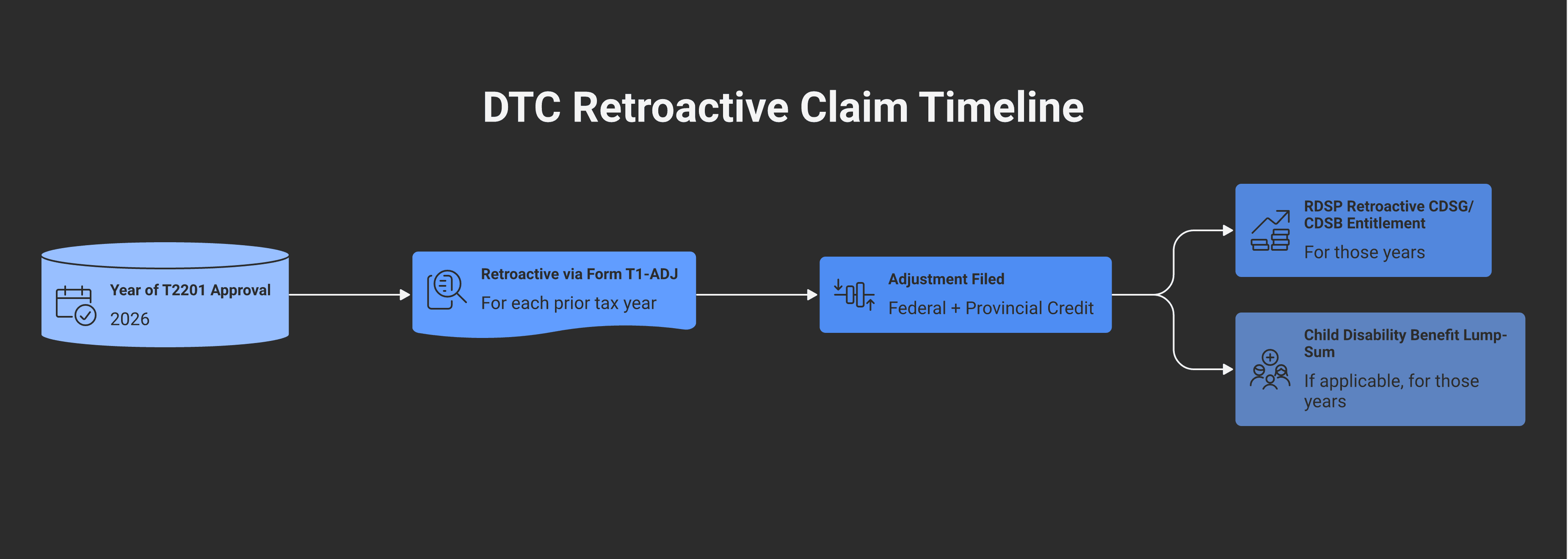

Retroactive claims — up to 10 years back

Approval is not just forward-looking. If the medical practitioner certifies on Form T2201 that the impairment existed in earlier tax years, CRA will apply the credit retroactively to each of those years — up to a 10-year limit under the normal reassessment window.

The mechanism is Form T1-ADJ, T1 Adjustment Request, filed once for each prior year that the credit should be applied to. A 10-year retroactive claim for a newly approved applicant who has been impaired for that period can produce a federal-and-provincial refund in the range of $20,000 to $25,000 — sometimes more if a supporting person was paying substantial tax and absorbed the full transferred amount each year.

Two important downstream effects of retroactive approval:

RDSP retroactive contributions. If the beneficiary's DTC is approved retroactively for prior years, the Canada Disability Savings Grant and Bond are payable for those prior years up to the lifetime caps — provided the RDSP is opened and contributions made within the timing rules. This can pull tens of thousands of dollars of government grants into the plan in one year.

CCB Child Disability Benefit retroactive. A retroactive DTC approval for a child triggers retroactive payment of the Child Disability Benefit for those prior years, typically paid as a lump sum after the T2201 is approved.

The retroactive piece is the part most families miss when they apply themselves or use a non-CPA application service. Practitioners often default to certifying "current year only" because the form gives them no obvious cue to certify back to a date of onset.

Why applications get denied — and how to fix them

Most denials trace back to four specific Part B issues. The good news: these are fixable. After a denial, the applicant has 90 days to file a Notice of Objection or request a Letter of Review with new information from the practitioner. We cover the objection process in detail in our forthcoming post on CRA dispute mechanics.

Denial reason 1: marked-restriction language not used. The practitioner described the impairment but did not use CRA's required language — "markedly restricted," "all or substantially all of the time," "even with therapy, medication, and devices." CRA reads for these phrases. Without them, the assessor cannot tick the box.

Denial reason 2: inordinate time not quantified. "Patient has difficulty walking" is not enough. "Patient takes 15 minutes to walk 100 metres where an unimpaired adult takes 90 seconds — at least 10 times longer" is enough. The practitioner needs to state the time multiple, not just say "inordinate."

Denial reason 3: prolonged not specified. The form requires the practitioner to state the date the impairment began and whether it has lasted (or is expected to last) at least 12 months. A blank or "unknown" entry triggers denial.

Denial reason 4: cumulative effect not built. Where no single activity is markedly restricted but two or more are significantly restricted, the practitioner must explicitly state each significant restriction and conclude that the cumulative effect is equivalent to a marked restriction in one activity. Practitioners frequently complete the individual sections but skip the conclusion — and CRA cannot assemble it themselves.

When a denial comes back, the practical move is: get a copy of the Notice of Determination from the CRA, identify which category the assessor focused on, then return to the practitioner with the specific language and quantification CRA needs, and submit a Letter of Review with the revised Part B. The 90-day window starts on the date of the Notice; missing it forces a new T2201 submission rather than a review of the existing one.

Common situations

Adult child with autism spectrum disorder, supporting person claims the credit. If the adult child has no taxable income, the credit transfers to a supporting parent or relative under subsection 118.3(2). The supporting person should also evaluate whether the Canada Caregiver Credit applies — these are two distinct credits, both can be claimed simultaneously, and DTC approval substantiates the marked-impairment requirement for the caregiver credit. Families with adult dependants should also look at the broader income-splitting toolkit — DTC approval expands several of the credits that work alongside split-income planning.

Aging parent with cognitive decline (early-stage dementia). Mental functions for everyday life is the relevant category. The key practitioner detail: memory, problem-solving, and adaptive functioning are each separate components — a careful Part B addresses each one. Many denials in this scenario come from practitioners writing about diagnosis (Alzheimer's, vascular dementia) without translating the diagnosis into the functional restrictions CRA wants to see.

Child with severe learning disability or ADHD. Mental functions, often with a cumulative-effect angle. The supplement for children under 18 ($6,032 for 2026) makes the approval economically meaningful — and the retroactive piece, if the diagnosis traces back several years, can pull substantial credits forward.

Adult with Type 1 diabetes. Automatically deemed to meet the 14-hour life-sustaining therapy threshold under subsection 118.3(1.2). The practitioner needs to confirm the Type 1 diagnosis on Part B — the form was updated in 2024 to simplify this — but no hour logging is required.

Cross-border filer. US persons living in Canada often have their tax planning structured around the Foreign Earned Income Exclusion and treaty positions, but the Canadian DTC remains available so long as the person is a Canadian tax resident. The credit reduces Canadian tax; it does not affect US tax. For a US person whose Canadian tax is high (income above the FEIE), DTC approval can have a meaningful effect.

Planning around DTC approval

A few moves CPAs make once DTC approval is in hand:

Open the RDSP first. Before optimising anything else. Canada Disability Savings Bond is paid for low-income beneficiaries automatically once the plan is open; CDSG matching requires contributions but produces 100% to 300% match on the first $1,500 of family contributions per year depending on family income.

File the T1-ADJ adjustments for prior years immediately. Retroactive refunds at 10 prior years can run in the tens of thousands of dollars. There is no reason to wait — the file an adjustment for each year separately.

Re-examine the medical expense tax credit. With DTC approval, attendant care expenses become more clearly deductible (and the disability supports deduction becomes available for working-age individuals).

Coordinate with the Canada Caregiver Credit and Home Accessibility Tax Credit annually. Neither is automatic — both must be claimed each year on the supporting person's return.

Watch the determination expiry. CRA typically grants approval for 5 or 10 years. Plan the re-certification a few months before expiry to avoid a gap.

For families with a child or adult dependant with a long-term disability, the DTC stack — the credit itself plus the RDSP plus the CDB plus the CCC plus the HATC — is often the single most consequential piece of long-term tax planning. It also interacts with family trust planning where a Henson trust or a regular discretionary trust is used to hold assets for a beneficiary with a disability. At Modern Axis, we frequently see families who have qualified for years on paper but never had the T2201 properly filed and end up walking away with retroactive refunds plus a freshly opened RDSP within a single tax cycle.

If you are weighing whether you or a family member would qualify, or you have been denied and want a CPA's read on whether the Part B can be rebuilt, tax planning support at Modern Axis routinely covers DTC strategy alongside the RDSP, CDB, and caregiver credit stack. Most of the value sits in getting the application right the first time and pulling the retroactive years forward — both of which compound over a working lifetime.

Frequently asked questions

How much is the disability tax credit worth in Canada for 2026?

For 2026, the federal disability amount is $10,341, producing approximately $1,448 of federal tax reduction at the 14% lowest rate (down from 15% as of July 1, 2025). Children under 18 receive an additional federal supplement of $6,032 (about $844 federal tax reduction, reduced dollar-for-dollar by attendant care or child care claims exceeding $3,533). Every province except Quebec adds its own parallel credit, bringing combined federal-plus-provincial value to roughly $2,000 to $2,400 per year for most adults under subsection 118.3(1) of the Income Tax Act.

Can I claim the disability tax credit retroactively?

Yes. If the medical practitioner certifies on Form T2201 that the impairment existed in earlier tax years, CRA will apply the credit retroactively for up to 10 prior tax years. Each prior year is adjusted via Form T1-ADJ, T1 Adjustment Request. Retroactive approval also triggers retroactive RDSP grant entitlement and retroactive Child Disability Benefit payments where applicable.

Who can certify Form T2201?

The authorised practitioner depends on the category. Medical doctors and nurse practitioners can certify any category. Optometrists certify vision; audiologists certify hearing; speech-language pathologists certify speech; occupational therapists certify walking, feeding, and dressing; psychologists certify mental functions; and physiotherapists can certify walking. These categories are set in subsections 118.3(1)(a.2) and (a.3) of the Income Tax Act.

Does Type 1 diabetes automatically qualify for the disability tax credit?

Yes. Subsection 118.3(1.2), added by Parliament in 2022, deems individuals with Type 1 diabetes to require life-sustaining therapy meeting the 14-hour-per-week threshold. The medical practitioner only needs to confirm the Type 1 diagnosis on Part B — no time logs or step-by-step administration documentation are required. Type 2 diabetes is not covered by the deeming provision and must qualify under the standard 14-hour rules if at all.

Why was my DTC application denied?

Most denials come from how the medical practitioner completed Part B — not from whether the impairment qualifies. The four common patterns are: not using the language "markedly restricted" and "all or substantially all of the time," not quantifying inordinate time as a specific multiple, not stating the date the impairment began and that it has lasted at least 12 months, and not explicitly building the cumulative-effect conclusion where it applies. After a denial, applicants have 90 days to submit a Letter of Review with a revised Part B from the practitioner.

What is the difference between the disability tax credit and the Canada Disability Benefit?

The disability tax credit reduces income tax payable; the Canada Disability Benefit pays a monthly amount of up to $200 directly. The DTC is governed by section 118.3 of the Income Tax Act; the CDB is governed by the Canada Disability Benefit Act. An approved Form T2201 is a prerequisite for both — without DTC approval, the CDB application cannot be processed.

Can the disability tax credit be transferred to a family member?

Yes, under subsection 118.3(2). If the person with the impairment has insufficient income to use the credit, it transfers to a supporting spouse, parent, grandparent, child, sibling, aunt, uncle, niece, or nephew. The supporting person claims the credit on their own return. Most families with a child or adult dependant with a disability claim the credit on the supporting person's return for this reason.

This article is for general information only and does not constitute professional tax, accounting, or legal advice. Every tax situation is different, and a blog post — no matter how detailed — cannot account for the specific facts that may change the analysis for you. Before acting on anything you've read here, speak with a qualified tax professional about your own circumstances.

Alex Ataman, CPA

Founder

Modern Axis CPA