Canada Tax Brackets 2026: Federal and Provincial Rates

The most consequential change to the Canada tax brackets in 2026 is not a new bracket or a new credit. It is the drop in the lowest federal rate from 15% to 14%, which took effect July 1, 2025 and now applies for the full 2026 tax year. Every non-refundable credit that ties to the lowest rate — the basic personal amount, the age amount, the disability amount, the spousal credit, the Canada caregiver credit, charitable donations under $200, medical expenses — is now worth a touch less per dollar of underlying amount.

The lowest-bracket rate cut is partially offset by the 2.0% indexation of bracket thresholds and credit amounts (down from 2.7% in 2025), so for most filers the headline change is a small net reduction in tax. But for high earners, the integration math behind dividends shifts visibly, and for owner-managers planning compensation between salary and dividends the choice tilts slightly toward dividends.

This guide walks through the Canada tax brackets 2026 in full — the federal schedule, all 13 provincial and territorial schedules, the combined top marginal rates by income type, the indexation mechanism, the basic personal amount rules, and the planning implications that follow.

Key takeaways

For 2026, federal marginal rates are 14%, 20.5%, 26%, 29%, and 33% under section 117 of the Income Tax Act. The lowest rate dropped from 15% to 14% effective July 1, 2025 and applies for the full 2026 calendar year.

Federal bracket thresholds for 2026 are $58,523, $117,045, $181,440, and $258,482, indexed by 2.0% from 2025.

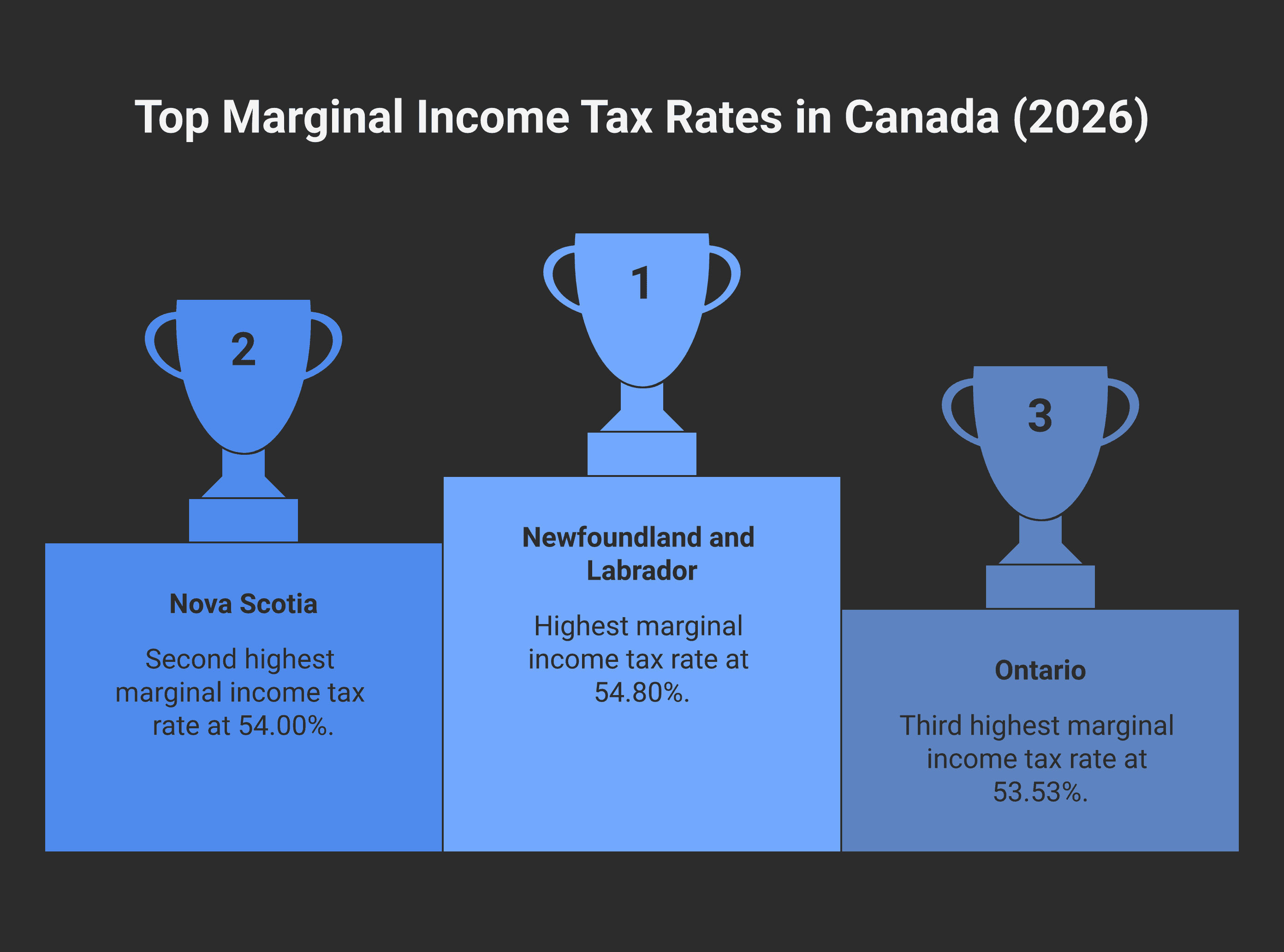

The combined federal-plus-provincial top marginal rate on ordinary income in 2026 ranges from about 44.5% in Nunavut to about 54.8% in Newfoundland and Labrador. British Columbia's top combined rate is approximately 53.5%; Ontario's is 53.53%; Alberta's is 48.0%; Quebec's is 53.31%.

Different income types are taxed at very different rates at the top. For an Ontario resident in the top federal bracket in 2026: ordinary income at 53.53%, capital gains at 26.76%, eligible dividends at 39.34%, non-eligible dividends at 47.74%.

The federal basic personal amount for 2026 is between $14,829 and $16,452 — phased down for taxpayers whose income falls in the second-highest federal bracket. Non-refundable credits tied to the lowest rate are now multiplied by 14%, not 15%.

The federal schedule for 2026

Federal personal tax is structured as a progressive five-bracket schedule under section 117. For 2026:

Taxable income | Federal rate |

|---|---|

Up to $58,523 | 14% |

$58,523 to $117,045 | 20.5% |

$117,045 to $181,440 | 26% |

$181,440 to $258,482 | 29% |

Above $258,482 | 33% |

The rate on the first bracket dropped to 14% effective July 1, 2025 (a 2025 measure of the new government — announced by the Department of Finance on May 14, 2025 and confirmed by Prime Minister Mark Carney on June 30, 2025, not part of Budget 2024), and applies in full for the 2026 tax year and beyond. Mechanically, the 2025 transitional year used a blended rate (14.5%) because the change happened mid-year. For 2026, the rate is a clean 14%.

Bracket thresholds are adjusted each year by the federal indexation factor — the 12-month change in the Consumer Price Index measured to September of the prior year. For 2026, the indexation factor is 2.0% (compared to 2.7% in 2025).

Provincial and territorial schedules

Every province and territory has its own personal income tax schedule, layered on top of federal tax. Quebec is the only jurisdiction that collects its own tax directly (administered by Revenu Québec, not the CRA); every other province uses the federal collection system but applies its own brackets and rates.

Provincial bracket thresholds are also indexed each year (most provinces use their own indexation factor, which may differ from the federal 2.0%). Several provinces have made discretionary changes for 2026:

British Columbia: Lowest provincial bracket rate increased from 5.06% to 5.6% for 2026. Other brackets unchanged.

Newfoundland and Labrador: Top bracket rate remains the highest in the country at 21.8% provincial — combined with the federal 33%, this produces the highest combined ordinary-income rate in Canada.

Alberta: Bracket structure remains simple — flat 10% provincial up to about $151K, then four tiers from 12% to 15%. No 2026 rate changes.

Ontario: Provincial surtax structure (20% / 36%) continues to compound the top marginal rates beyond the headline rates.

Combined top marginal rates by province (2026)

The most commonly referenced figure when comparing provincial tax burdens is the combined federal-plus-provincial top marginal rate on ordinary income. For 2026:

Province/Territory | Top combined rate on ordinary income | Income threshold where top rate starts |

|---|---|---|

Newfoundland and Labrador | 54.80% | $1,128,858 |

Nova Scotia | 54.00% | $258,482 |

Prince Edward Island | 51.37% | $258,482 |

New Brunswick | 52.50% | $258,482 |

Ontario | 53.53% | $258,482 |

Quebec | 53.31% | $258,482 |

Manitoba | 50.40% | $258,482 |

Saskatchewan | 47.50% | $258,482 |

Alberta | 48.00% | $370,221 |

British Columbia | 53.50% | $265,545 |

Yukon | 48.00% | $500,000 |

Northwest Territories | 47.05% | $258,482 |

Nunavut | 44.50% | $258,482 |

The income threshold at which the top combined rate kicks in varies because each province's top bracket threshold differs from the federal $258,482 threshold. Alberta's top rate only applies above $370,221; BC's above $265,545; Yukon's above $500,000. For most other jurisdictions the federal threshold drives the top combined rate.

Rates by income type — the integration view

The headline marginal rate matters less than the rate by income type. The Canadian tax system applies a 50% capital gains inclusion rate (under section 38 of the Income Tax Act) and provides the dividend tax credit for both eligible and non-eligible dividends — both designed to integrate corporate and personal taxation so that the total tax on a dollar of corporate income equals roughly the personal tax on the same dollar earned directly.

For a high-income filer in each major province in 2026, the combined federal-and-provincial top rates by income type look like this:

Province | Ordinary income | Capital gains | Eligible dividends | Non-eligible dividends |

|---|---|---|---|---|

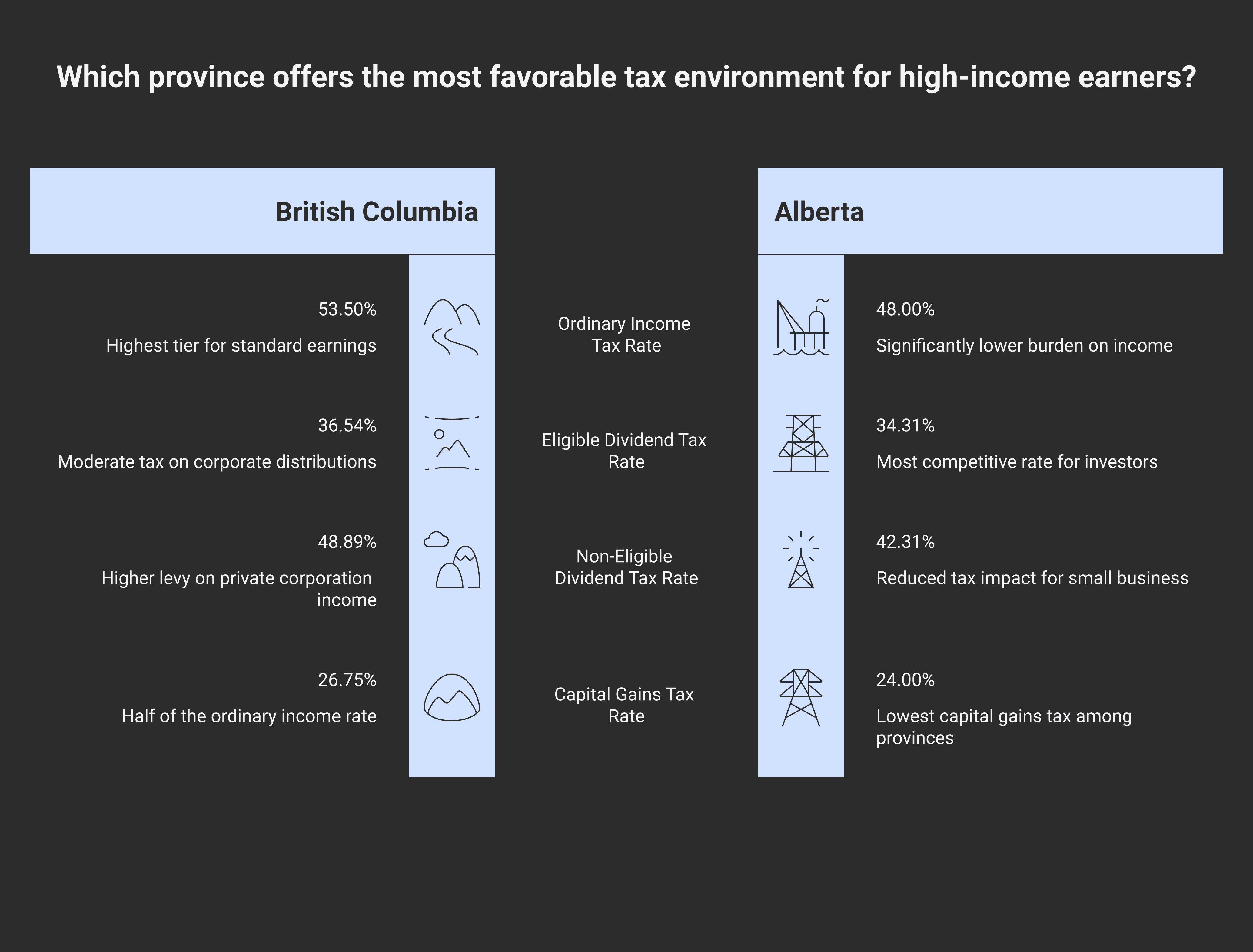

British Columbia | 53.50% | 26.75% | 36.54% | 48.89% |

Alberta | 48.00% | 24.00% | 34.31% | 42.31% |

Saskatchewan | 47.50% | 23.75% | 29.64% | 41.34% |

Manitoba | 50.40% | 25.20% | 37.78% | 46.67% |

Ontario | 53.53% | 26.76% | 39.34% | 47.74% |

Quebec | 53.31% | 26.65% | 40.11% | 48.70% |

New Brunswick | 52.50% | 26.25% | 32.40% | 46.83% |

Nova Scotia | 54.00% | 27.00% | 41.58% | 48.27% |

PEI | 51.37% | 25.69% | 36.20% | 47.63% |

Newfoundland and Labrador | 54.80% | 27.40% | 46.20% | 48.96% |

Yukon | 48.00% | 24.00% | 28.92% | 44.05% |

Northwest Territories | 47.05% | 23.53% | 28.33% | 36.82% |

Nunavut | 44.50% | 22.25% | 33.08% | 37.79% |

The capital gains rate is always exactly half the ordinary-income rate, by design (50% of the gain is included in income, taxed at the full marginal rate).

The eligible dividend rate is consistently lower than non-eligible because eligible dividends are paid out of corporate profits taxed at the higher general corporate rate (no SBD benefit), and the gross-up plus dividend tax credit reflects that.

Our deep dive on eligible vs non-eligible dividends covers the integration math — the GRIP/LRIP pools, the Schedule 53 mechanics — that drives the difference between those two columns. For owner-managers choosing how to pay themselves, the income-type column matters more than the headline ordinary-income column.

The basic personal amount

The federal basic personal amount is a non-refundable credit that effectively zeroes out tax on the first chunk of income for low and middle earners. For 2026 it ranges from a minimum of $14,829 to a maximum of $16,452.

The reason there is a range: the basic personal amount was increased to a higher maximum for taxpayers in the lowest federal brackets and phased down for high earners. The phase-down works as follows:

Taxpayers with net income at or below the second-highest federal bracket threshold ($181,440 for 2026) receive the full $16,452.

Between $181,440 and $258,482, the BPA phases down linearly.

Above $258,482, the BPA settles at the floor of $14,829.

Multiplied by the 14% lowest rate in 2026:

Maximum BPA tax reduction: $16,452 × 14% = $2,303

Minimum BPA tax reduction: $14,829 × 14% = $2,076

Most other non-refundable credits work the same way — multiply the underlying amount by 14% to get the federal tax reduction. Provincial parallel credits use each province's lowest rate, layered on top.

A non-exhaustive list of credits tied to the lowest rate in 2026:

Basic personal amount, spouse or common-law partner amount, eligible dependant amount

Age amount (for filers 65+)

Canada caregiver credit

Disability amount and supplement (see our disability tax credit guide)

Pension income amount

Tuition tax credit (transferred or carried forward)

First-time home buyers' credit

Home accessibility tax credit

Charitable donations on the first $200 (after $200, the rate is the top federal rate of 33% for high earners)

Medical expenses (above 3% of net income or $2,890 for 2026, whichever is less)

The shift from 15% to 14% means each of these credits is now worth 6.67% less in federal tax reduction per dollar of underlying amount than it was in 2024.

What's changed vs 2025

The major changes that distinguish 2026 from 2025:

Item | 2025 | 2026 |

|---|---|---|

Lowest federal rate | 14.5% (transitional) | 14% (full year) |

Federal indexation factor | 2.7% | 2.0% |

First bracket top | $57,375 | $58,523 |

Second bracket top | $114,750 | $117,045 |

Third bracket top | $177,882 | $181,440 |

Fourth bracket top | $253,414 | $258,482 |

Basic personal amount (max) | $16,129 | $16,452 |

BC lowest provincial rate | 5.06% | 5.6% |

Capital gains inclusion rate remains at 50% for individuals (the proposed move to 66.67% for gains above $250,000 announced in Budget 2024 was deferred in January 2025, then cancelled in Budget 2025 in March 2025 — see our coverage of the saga). The AMT structure remains as restructured by Budget 2024's reforms.

Planning implications

A few moves that follow from the 2026 schedule:

Timing income recognition. Income that can be deferred from one year to the next is more valuable when bracket thresholds are rising and the lowest rate is lower. RRSP withdrawals planned in retirement, capital gains realisation, bonus timing, and CCPC dividend declarations are the usual levers.

Re-examine salary-versus-dividend. The drop in the lowest federal rate makes dividend income marginally more attractive relative to salary at the bottom of the salary recipient's bracket. The integration math for an Ontario owner-manager paying themselves $58,523 (the top of the 14% bracket) is meaningfully different than it was at 15%.

Re-examine the donation strategy. The donation credit jumps from 14% on the first $200 to the top federal rate of 33% on the excess (for high-income filers). The 1% gap at the bottom is small, but for a filer giving more than $200 the math doesn't change much.

Pension income splitting (after 65). Pension income up to 50% can be allocated to a lower-income spouse under section 60.03 of the Income Tax Act. With the 14% bottom-bracket rate, the split saves slightly less per dollar than it did at 15% — but the structural value is unchanged.

The DTC, RDSP, and disability credit stack. For families with a child or adult dependant with DTC approval, the credit math runs slightly leaner at 14%, but the RDSP grant matching is unaffected — that's the dominant program and the change is immaterial there.

TFSA and RRSP contribution room. The 2026 TFSA dollar limit remains at $7,000 — the indexed value rounded to the nearest $500 has not yet crossed the threshold to bump to $7,500 (the next jump is expected in 2027). The 2026 RRSP contribution limit is $33,810, applicable to taxpayers with 18% of prior-year earned income reaching that cap (earned income of approximately $187,833 in 2025).

For most high-income filers, the structural moves around the 2026 brackets are the same ones that always matter: defer realisation of fully taxable income, harvest capital losses against gains, top up tax-advantaged accounts, and coordinate corporate dividends with the personal bracket. At Modern Axis, we run combined federal-provincial tax projections for clients each fall before year-end so the salary, dividend, and bonus mix is sized to where the brackets actually break — not where they were last year.

Frequently asked questions

What are the federal tax brackets in Canada for 2026?

For 2026 the federal brackets are 14% on the first $58,523, 20.5% on $58,523 to $117,045, 26% on $117,045 to $181,440, 29% on $181,440 to $258,482, and 33% on income above $258,482. The lowest rate dropped from 15% to 14% effective July 1, 2025 and applies for the full 2026 tax year under section 117 of the Income Tax Act. Bracket thresholds are indexed annually by the federal indexation factor (2.0% for 2026).

What is the highest combined tax rate in Canada in 2026?

Newfoundland and Labrador has the highest combined federal-and-provincial top marginal rate on ordinary income at approximately 54.80% in 2026. Nova Scotia is second at 54.00%, followed by Ontario at 53.53% and British Columbia at 53.50%. The lowest combined top rate is Nunavut at approximately 44.50%. Alberta sits at 48.00% on ordinary income but its top bracket starts at $370,221 rather than the federal threshold of $258,482.

Why did the lowest federal tax rate drop from 15% to 14% in 2026?

The lowest federal rate was reduced from 15% to 14% effective July 1, 2025, as a middle-class tax relief measure of the new government — announced by the Department of Finance on May 14, 2025 and confirmed by Prime Minister Mark Carney on June 30, 2025, not in Budget 2024. The 2025 transitional year used a blended rate of 14.5% because the change took effect mid-year. For 2026 the full 14% rate applies, reducing federal tax for every filer with taxable income in the lowest bracket.

How are capital gains taxed in 2026?

Capital gains are taxed at the filer's marginal rate on 50% of the gain under section 38 of the Income Tax Act. The 2024 proposal to increase the inclusion rate to 66.67% for gains above $250,000 was deferred in January 2025 and cancelled in Budget 2025 in March 2025. For 2026 the inclusion rate remains 50% for both individuals and corporations.

What is the basic personal amount in Canada for 2026?

The federal basic personal amount for 2026 ranges from $14,829 to $16,452, depending on the filer's net income. Filers with net income at or below $181,440 receive the full $16,452. Between $181,440 and $258,482, the amount phases down linearly. Above $258,482, the amount settles at $14,829. Multiplied by the 14% lowest federal rate, the maximum BPA produces approximately $2,303 of federal tax reduction.

How are eligible and non-eligible dividends taxed differently in 2026?

Eligible dividends (paid from corporate income taxed at the higher general corporate rate, tracked in the GRIP pool) and non-eligible dividends (paid from corporate income taxed at the lower small business deduction rate, tracked in LRIP) are grossed up and credited at different rates to maintain integration. For a top-bracket Ontario filer in 2026, eligible dividends are taxed at approximately 39.34% combined and non-eligible dividends at approximately 47.74%. The difference reflects the lower corporate-level tax already paid on the underlying SBD income for non-eligible dividends.

What is the TFSA contribution limit for 2026?

The TFSA dollar limit for 2026 remains $7,000, unchanged from 2024 and 2025. Although the limit is indexed to inflation, it is rounded to the nearest $500 — the indexed value has not yet crossed the threshold required to bump to $7,500 (that increase is now expected for 2027). Unused contribution room carries forward indefinitely. A Canadian resident who turned 18 in 2009 and has been resident since has cumulative TFSA contribution room of approximately $109,000 as of 2026.

This article is for general information only and does not constitute professional tax, accounting, or legal advice. Every tax situation is different, and a blog post — no matter how detailed — cannot account for the specific facts that may change the analysis for you. Before acting on anything you've read here, speak with a qualified tax professional about your own circumstances.

Alex Ataman, CPA

Founder

Modern Axis CPA