Eligible vs Non-Eligible Dividends: GRIP, LRIP Explained

If you own a Canadian-controlled private corporation and you are paid in dividends, the after-tax dollar you receive depends on what kind of dividend it is. Two types exist: eligible and non-eligible. They are taxed at different personal rates, carry different dividend tax credits, and come from different pools inside the corporation. Owner-managers who don't know which pool their dividend is being drawn from often pay materially more personal tax than the integration math intended.

Key takeaways

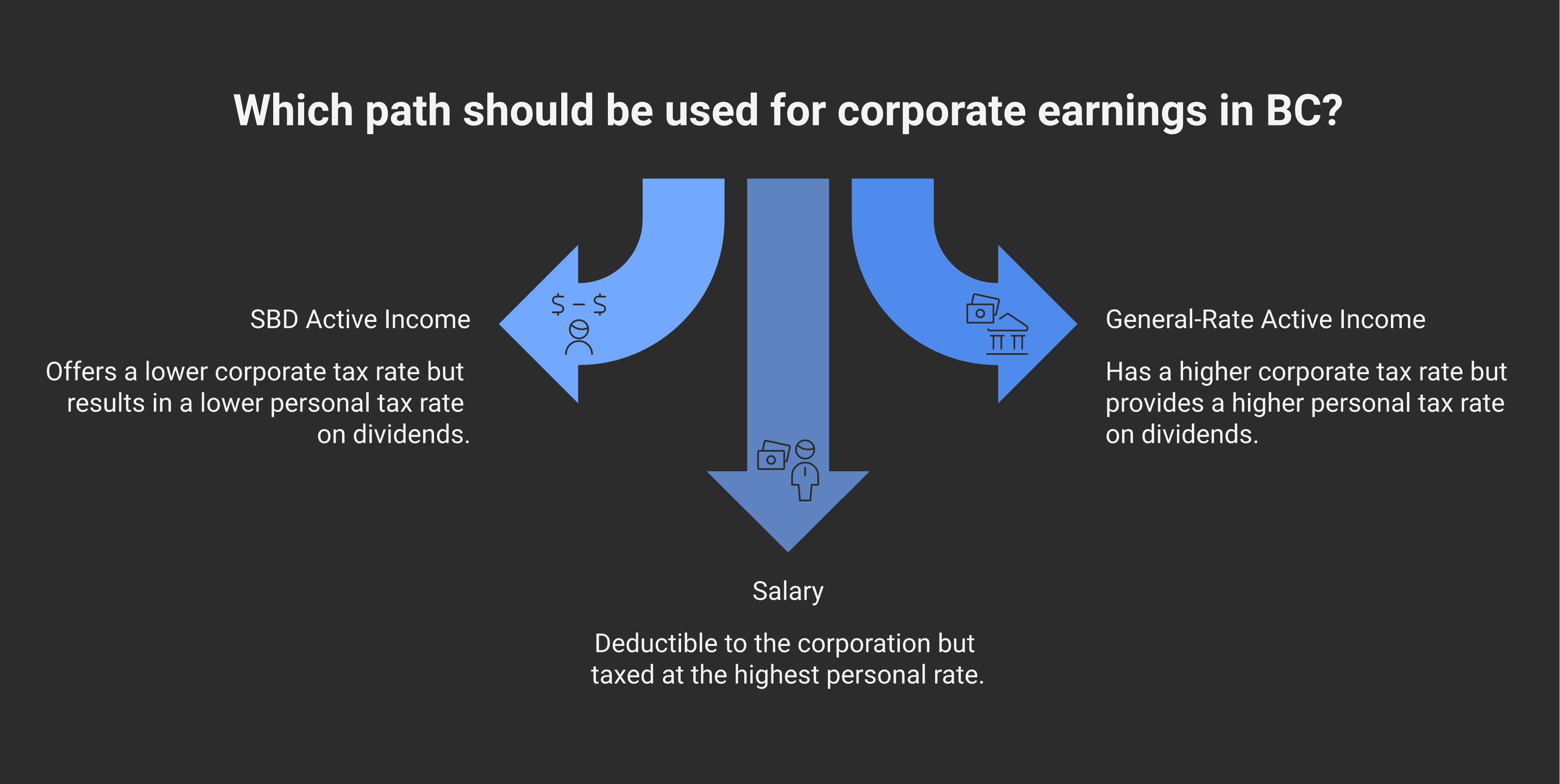

Eligible dividends flow from corporate income taxed at the general rate (~27% combined in BC) and carry a 38% gross-up plus 15.02% federal dividend tax credit — lower personal tax than non-eligible.

Non-eligible dividends flow from small-business-deduction income (~11% combined in BC), carry a 15% gross-up and 9.03% federal dividend tax credit — higher personal tax than eligible.

A CCPC's GRIP (General Rate Income Pool) tracks how much it can distribute as eligible dividends; LRIP is the mirror image for non-CCPCs, where dividends are eligible by default unless LRIP is reduced first.

Excess eligible dividend designations (greater than GRIP) trigger Part III.1 tax under section 185.1 at 20% of the excess, with a 90-day recharacterisation election as the only escape.

This post is about how Canada's dividend integration system works, what the General Rate Income Pool (GRIP) and Low Rate Income Pool (LRIP) actually track, how the section 89(14) eligible dividend election is made, what happens when an eligible dividend exceeds the GRIP balance, and where the integration breaks down in practice.

The rule, in one sentence

Under section 89, every taxable dividend paid by a Canadian corporation is either an "eligible dividend" or a "non-eligible dividend" — eligible dividends carry a higher gross-up and a higher tax credit, reflecting that the underlying corporate income was already taxed at the general rate; non-eligible dividends carry a lower gross-up and a lower tax credit, reflecting that the underlying corporate income benefited from the lower small business rate; CCPCs use the GRIP balance to designate eligible dividends, non-CCPCs are constrained by the LRIP balance.

The point of the two-tier system is tax integration: the combined corp + personal tax on $1 should roughly equal what an individual would have paid earning $1 directly. The system works imperfectly — there are gaps and surpluses depending on province, dividend type, and the corporate income pool the dividend is drawn from. (Modern Axis's salary-vs-dividends post covers the broader owner-compensation decision.)

Two tax pools, two dividend types

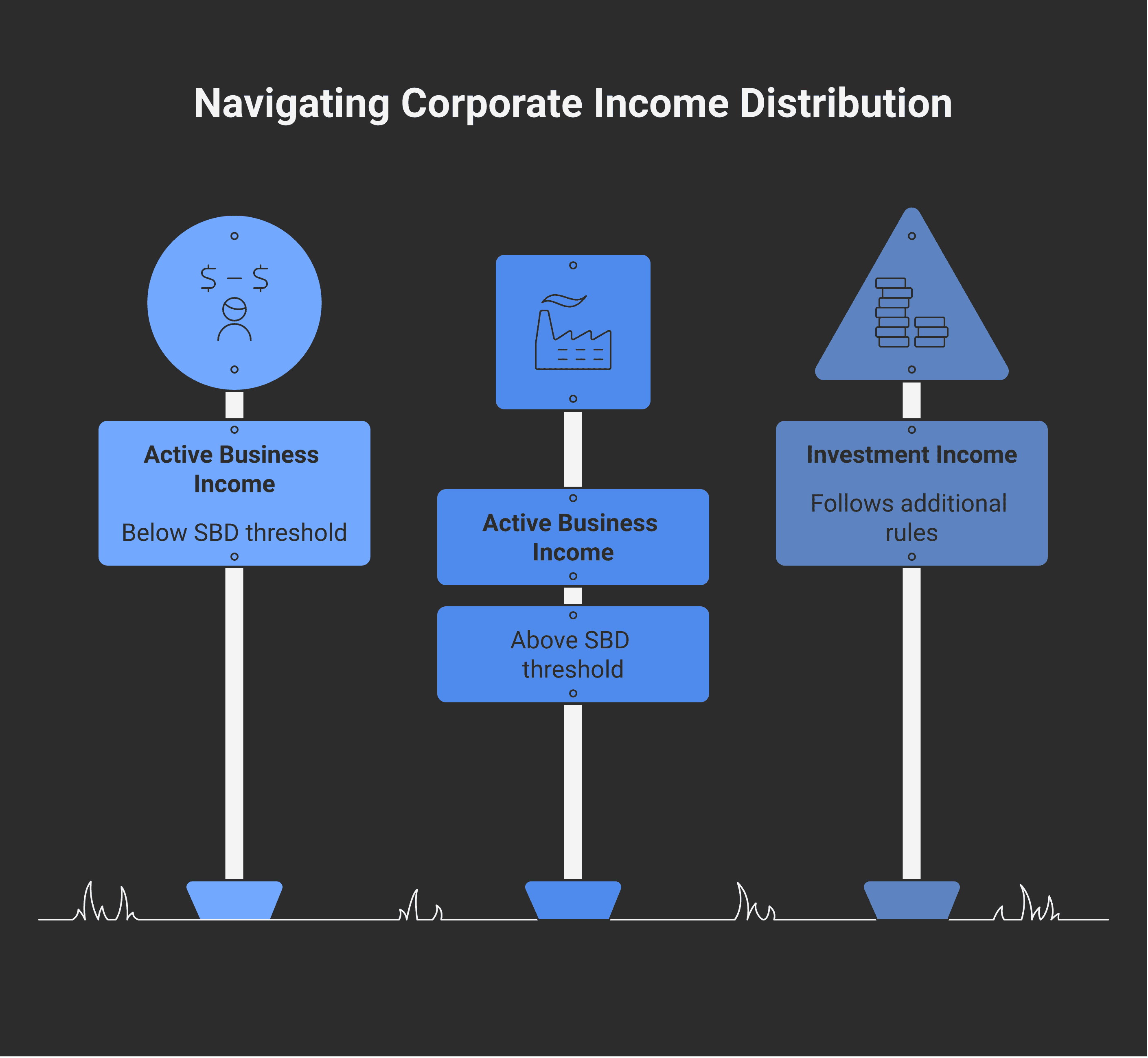

The active business income split

A CCPC's first $500,000 of active business income each year is eligible for the small business deduction under section 125 of the Income Tax Act, which reduces the combined federal+provincial corporate tax rate to roughly 11% in BC (varies by province). Active business income above the $500,000 threshold is taxed at the full general corporate rate of roughly 27% in BC.

When the corporation eventually distributes these earnings:

Income taxed at the low (SBD) rate flows out as a non-eligible dividend — small gross-up, small tax credit, higher personal rate

Income taxed at the high (general) rate flows out as an eligible dividend — large gross-up, large tax credit, lower personal rate

The personal rates are calibrated so that the combined tax (corp + personal) is roughly equal whichever pool the income came from. Owner-managers who only realise they have two pools to draw from after years of cumulative GRIP buildup are often surprised at how much eligible-dividend room they've banked.

Investment income — refundable taxes

Investment income inside a CCPC follows a different mechanic. Passive income (interest, foreign dividends, rents, capital gains) is taxed at a high corporate rate with a refundable component. The taxes paid create balances in eRDTOH and nRDTOH (eligible and non-eligible refundable dividend tax on hand) which are recovered by the corp when it later pays dividends. This piece is covered in Modern Axis's holdco investment income post; for the purposes of this post, treat investment income's eventual dividend distribution as typically non-eligible.

The General Rate Income Pool (GRIP)

For a CCPC, GRIP is a notional running balance that tracks the corporation's accumulated general-rate income — meaning income that was taxed at the corporate rate above the small business rate. GRIP grows from:

Active business income above the $500,000 SBD threshold (i.e., income that didn't get the SBD reduction)

Investment income (after the refundable-tax mechanics) — though much of this is captured in the LRIP-equivalent calculation

GRIP additions from other corporations (eligible dividends received)

GRIP shrinks when:

Eligible dividends are paid out (one-for-one reduction)

Excess eligible-dividend designations are recharacterised under section 185.1(3)

The annual GRIP addition formula is in subsection 89(1) — schematically:

GRIP at end of year = GRIP at start of year + (current year general-rate factor × current year taxable income) − eligible dividends paid in the year

The "general-rate factor" is set annually and is approximately the difference between the general corporate rate and the small business rate. The actual T2 calculation is done on Schedule 53 — Calculation of General Rate Income Pool (GRIP). Year-end is when this gets calculated and reconciled.

What "designating" a dividend as eligible means

Under subsection 89(14), a corporation pays an eligible dividend by designating the dividend as eligible in writing to each shareholder (or by posting the designation publicly on the corporation's website) at the time the dividend is paid. The designation:

Has to be made on or before the time the dividend is paid

Is irrevocable

Cannot exceed the corporation's GRIP balance at the time

If the designation is missing or late, the dividend is treated as non-eligible (regardless of the corporation's GRIP balance). For private corps, the standard practice is for the directors' resolution authorising the dividend to include the eligible-dividend designation explicitly.

Excess designations and Part III.1 tax

If a CCPC designates more eligible dividends than its GRIP balance, the excess triggers Part III.1 tax under section 185.1 at 20% of the excess. (The same logic as the Part III tax on excess capital dividend elections, but at a less punitive rate — 20% rather than 60%.)

The escape: under subsection 185.1(2), within 90 days of the assessment (or earlier with notice), the corporation may elect with shareholder consent to recharacterise the excess as an ordinary (non-eligible) taxable dividend. The recharacterised amount is then taxable to the shareholder at non-eligible rates, but Part III.1 tax is avoided.

The Low Rate Income Pool (LRIP)

LRIP applies to non-CCPCs — public corporations, foreign-controlled corporations, and any private corp that doesn't meet the CCPC tests. The mechanic is the mirror image of GRIP:

For a non-CCPC, every dividend is eligible by default (because the corp is presumed to have paid full general rate)

A non-CCPC's LRIP balance tracks any income that was not taxed at the general rate (e.g., investment income with refundable-tax effects, dividends received from CCPC's small-business pool)

Before paying an eligible dividend, the corporation must first reduce its LRIP balance with a non-eligible dividend equal to the LRIP balance

Failing to clear LRIP first means the eligible designation is recharacterised as non-eligible (the corp can't move eligible dividends out while LRIP sits unsettled)

In practice, LRIP rarely surfaces for owner-managed CCPCs — it's mostly relevant to public corporations and structures with multiple corporation types. Awareness matters most when a Canadian holdco receives dividends from a foreign corp (the foreign corp's LRIP-equivalent status flows through).

The integration math — what actually arrives in your pocket

Tax integration is the principle that the combined corp + personal tax on $1 of corporate earnings should roughly equal the personal tax on $1 of personally-earned income. In practice, the math works for the eligible dividend side reasonably well, and slightly less cleanly for the non-eligible dividend side. The result is that there are small but meaningful surpluses or gaps depending on the path.

The headline insight from the integration table: at the top personal bracket in BC, all three paths (SBD non-eligible dividend, general-rate eligible dividend, salary) land within a few cents of each other on a $1 of pre-tax corporate income. At lower personal brackets, the math diverges — non-eligible dividends become relatively favourable (because the personal rate falls faster than the credit), and salary becomes relatively unfavourable (CPP loading on the corp + employee side).

The practical implication for owner-managers:

A corp earning entirely under the $500,000 SBD threshold has only non-eligible dividends to distribute. The integration math works well at top brackets, less well at lower brackets — meaning a low-income spouse receiving non-eligible dividends is at a slight advantage relative to receiving the same amount as a non-eligible dividend.

A corp earning above the $500,000 SBD threshold builds GRIP each year and gains the option to pay eligible dividends. Eligible dividends are particularly valuable for shareholders at the top bracket (lower personal tax than non-eligible).

The eligible-dividend designation is a useful planning lever after the corp has built sufficient GRIP. Spreading designations across years can smooth the recipient shareholder's personal tax exposure.

Sequencing eligible and non-eligible dividends

When a CCPC has GRIP built up, the next planning question is when to pay eligible vs non-eligible dividends. Common patterns:

Pay non-eligible first to lower-bracket family members (under TOSI carve-outs — see the TOSI excluded shares post) to capture the low-bracket personal rate. The low-bracket recipient pays a small effective personal rate on the non-eligible portion, since the gross-up + credit nearly offsets at low brackets.

Save eligible dividends for the high-bracket recipient (typically the owner-manager themselves), where the eligible rate (~36%) beats the non-eligible rate (~49%). The personal-tax saving is meaningful.

Coordinate with Capital Dividend Account elections — capital dividends are paid tax-free and don't draw from GRIP or LRIP. Stacking capital + eligible + non-eligible dividends in the right sequence across multiple shareholders is a year-end planning exercise.

Time eligible dividends around major personal income years (a year with high employment income, or a large capital gain) to push the dividend into a lower marginal bracket.

These sequencing decisions are typically made at year-end alongside the corporate tax filing — when GRIP is reconciled, RDTOH balances are confirmed, and the directors' resolution package is prepared.

When the eligible/non-eligible question lands on Modern Axis

Modern Axis CPA maintains the GRIP and (where relevant) LRIP continuity schedules for every incorporated owner-manager client. Year-end dividend planning includes: GRIP reconciliation, sequencing the eligible/non-eligible/capital dividend mix across multiple shareholders, integration-math comparison with salary alternatives, and the directors' resolution language that locks in the section 89(14) designation. The Tax Planning & Compliance service covers the annual cycle; restructuring (share re-issues, family trust insertions, holdco additions) is its own engagement.

Frequently asked questions

What's the difference between eligible and non-eligible dividends in Canada?

Eligible dividends are paid from corporate income taxed at the general corporate rate (~27% combined in BC). Non-eligible dividends are paid from income that benefited from the small business deduction (~11% combined in BC). Eligible dividends carry a 38% gross-up and a higher dividend tax credit, so the personal tax rate is lower (~36% at the top BC bracket) than on non-eligible (~49%). The system is calibrated for rough tax integration — combined corporate plus personal tax should be similar regardless of path.

What is GRIP and how is it calculated?

GRIP — General Rate Income Pool — is a notional running balance every CCPC maintains under subsection 89(1). It tracks accumulated income taxed at the general corporate rate (typically active business income above the $500,000 SBD threshold). Each year's addition is roughly the general-rate factor times taxable income, less eligible dividends paid in the year. The running total is reported annually on Schedule 53. A positive GRIP means eligible dividends are available to designate.

How do I designate a dividend as eligible?

Under subsection 89(14), the corporation designates a dividend as eligible by notifying each shareholder in writing — or by posting the designation on the corporation's public website — at the time the dividend is paid. The directors' resolution authorising the dividend typically includes the eligible-dividend designation language. The designation must be made no later than when the dividend is paid, and once made it is irrevocable.

What happens if I designate more eligible dividends than my GRIP balance?

The excess triggers Part III.1 tax under section 185.1 at 20% of the excess. The escape is subsection 185.1(2) — within 90 days of the assessment, the corporation may elect (with shareholder consent) to recharacterise the excess as a non-eligible dividend, in which case it's taxable to the shareholder at non-eligible rates and Part III.1 tax is avoided. The 90-day window is strict; missing it locks in the 20% penalty.

What is LRIP and when does it apply?

Low Rate Income Pool — the mirror image of GRIP for non-CCPCs (public corporations, foreign-controlled corporations, and any private corporation that doesn't meet the CCPC tests). A non-CCPC's dividends are eligible by default; LRIP tracks any income that was NOT taxed at the general rate. Before paying an eligible dividend, the non-CCPC must first reduce its LRIP balance by paying non-eligible dividends. For owner-managed CCPCs, LRIP rarely surfaces.

Should owner-managers take eligible or non-eligible dividends?

It depends on the recipient's marginal bracket and the corporation's GRIP balance. Top-bracket recipients benefit from eligible dividends (lower personal rate than non-eligible). Lower-bracket recipients may pay roughly the same or even slightly more on eligible because the credit is non-refundable beyond the gross-up benefit. The corporation's GRIP balance constrains how much can be eligible. Most owner-managers blend the two over time, modelling year-by-year.