Inheritance Tax in Canada: What Actually Happens

Canada does not have an inheritance tax. There is no federal estate tax, no probate-level death tax on the value of the estate, and no per-province inheritance levy on the beneficiary. Most Canadians inheriting money receive it tax-free in their hands.

That answer is correct, and it is also incomplete. The actual mechanic — what happens when a Canadian dies — is the deemed disposition rule under subsection 70(5) of the Income Tax Act. Every capital property owned by the deceased is treated as having been sold at fair market value immediately before death. The resulting capital gains are taxed on the deceased's final (terminal) tax return. The estate pays the tax; the beneficiaries receive what's left.

In other words: the inheritance is tax-free to the recipient, but the estate has already paid tax on the embedded gains. That distinction surprises a lot of first-time executors and beneficiaries — especially when probate fees, the principal residence exemption, the spousal rollover, and (for dual citizens) US estate tax intersect.

This guide walks through what actually happens to a Canadian estate at death — the deemed disposition rule, the spousal rollover, the principal residence exemption on death, probate fees by province, and the US estate tax considerations that apply to dual citizens and US persons living in Canada.

Key takeaways

There is no inheritance tax in Canada. Beneficiaries do not pay tax on inherited cash, property, or other assets when they receive them. The income tax has already been paid by the estate before distribution.

Capital property is deemed disposed of at fair market value on death under subsection 70(5) of the Income Tax Act. The deemed gain is taxed on the deceased's terminal return. The estate's executor files the terminal return.

The spousal rollover under subsection 70(6) allows capital property to transfer to a surviving spouse or qualifying spousal trust at cost (no deemed disposition), deferring the tax until the surviving spouse's death or eventual sale.

Probate fees are levied by each province, ranging from no fee (Quebec for notarised wills) to 1.4% of estate value with no cap (BC). Probate fees are not income tax — they are a separate levy on the value of the estate.

Dual citizens and US persons living in Canada face the additional US federal estate tax. The 2026 exemption is $15 million USD per person following the One Big Beautiful Bill Act (OBBBA, July 2025), which permanently extended and increased the prior TCJA exemption. The amount is indexed from 2027.

The deemed disposition rule

When a Canadian dies, subsection 70(5) treats every capital property they owned as having been sold at fair market value immediately before death. The deemed proceeds:

For each asset, fair market value (FMV) at the moment of death

Minus the adjusted cost base (ACB) for that asset

Equals the deemed capital gain (or loss)

The capital gain is reported on the deceased's terminal tax return, taxed at the deceased's marginal rate that year. The 50% inclusion rate applies (the proposed 66.67% inclusion for gains above $250,000 was deferred in January 2025 and cancelled in Budget 2025 in March 2025).

Examples of what gets deemed-disposed at death:

Non-registered investment portfolios (stocks, ETFs, mutual funds outside registered accounts): each holding is treated as sold at FMV, generating a capital gain or loss

Real estate other than the principal residence (rental properties, vacation homes, US real estate, raw land)

Privately-held business shares, including QSBC shares

Personal-use property above the $1,000 ACB / $1,000 deemed proceeds threshold

What is NOT deemed-disposed:

Cash and bank accounts (no capital property)

Bonds and GICs with no embedded gain (already taxed on interest as accrued)

TFSA balances (no tax on growth ever)

Principal residence (the principal residence exemption typically eliminates the gain — see below)

Registered accounts work differently. Under subsection 70(2) and section 146, an RRSP or RRIF on death is generally collapsed and the full balance added to the deceased's terminal return as ordinary income — unless rolled over to a surviving spouse, financially-dependent child, or grandchild. The full-collapse treatment can produce a very large income tax bill, often the single largest line on the terminal return.

The spousal rollover — the cleanest deferral

Under subsection 70(6) of the Income Tax Act, capital property transferred to a surviving spouse or common-law partner (or to a qualifying spousal trust) at death is rolled over at the deceased's adjusted cost base — no deemed disposition, no capital gain triggered.

The mechanic:

The deceased's terminal return reports no capital gain on the rolled-over property.

The surviving spouse inherits the property at the deceased's ACB (not at FMV).

The embedded gain is preserved and will be realised when the surviving spouse sells the property or dies.

For most married couples with a non-registered investment portfolio, the spousal rollover defers the entire deemed-disposition tax bill from first death to second death. The cost: the surviving spouse inherits the lower ACB, so when they eventually sell the embedded gain is taxed in their hands.

The same mechanic applies to RRSPs and RRIFs: a surviving spouse can transfer the deceased's RRSP/RRIF balance into their own registered account on a tax-deferred basis under subsection 60(l). This is the single most common piece of estate planning advice that gets executed correctly — but the named-beneficiary designation must be on the deceased's plan for the rollover to happen automatically. If no beneficiary is named, the balance falls into the estate and is taxed on the terminal return.

Spousal trust requirements. Property going to a spousal trust qualifies for rollover treatment only if the trust meets the requirements of subsection 70(6): the surviving spouse is entitled to all the income of the trust during their lifetime, and no one else can receive any of the trust's capital before the spouse's death.

The principal residence exemption on death

The [principal residence exemption under paragraph 40(2)(b)](https://modernaxis.ca/blog/real-estate-tax-implications) eliminates capital gains on the deceased's principal residence at death. Mechanically, the deemed disposition still occurs under 70(5), but the gain is offset by the PRE.

Important considerations on death:

One principal residence per family unit per year. For a couple, only one home can be designated. If the deceased was widowed, all years are usable. If still married, the spouse must agree on the designation.

The PRE is a designation, not automatic. The executor must make the designation in the deceased's final return on Form T1255 or T2091.

Year-of-acquisition through year-of-death formula. If the home was the principal residence for every year of ownership, the gain is fully exempt. If only part of the period (e.g., the home was rented out for some years), the exemption is prorated.

For most Canadian estates, the principal residence transfers to the surviving spouse via spousal rollover, with the PRE preserved for the surviving spouse's eventual sale or death. For unmarried decedents, the PRE typically eliminates the deemed gain on the family home at death, leaving the home to pass to beneficiaries with a stepped-up cost base equal to the FMV at the date of death.

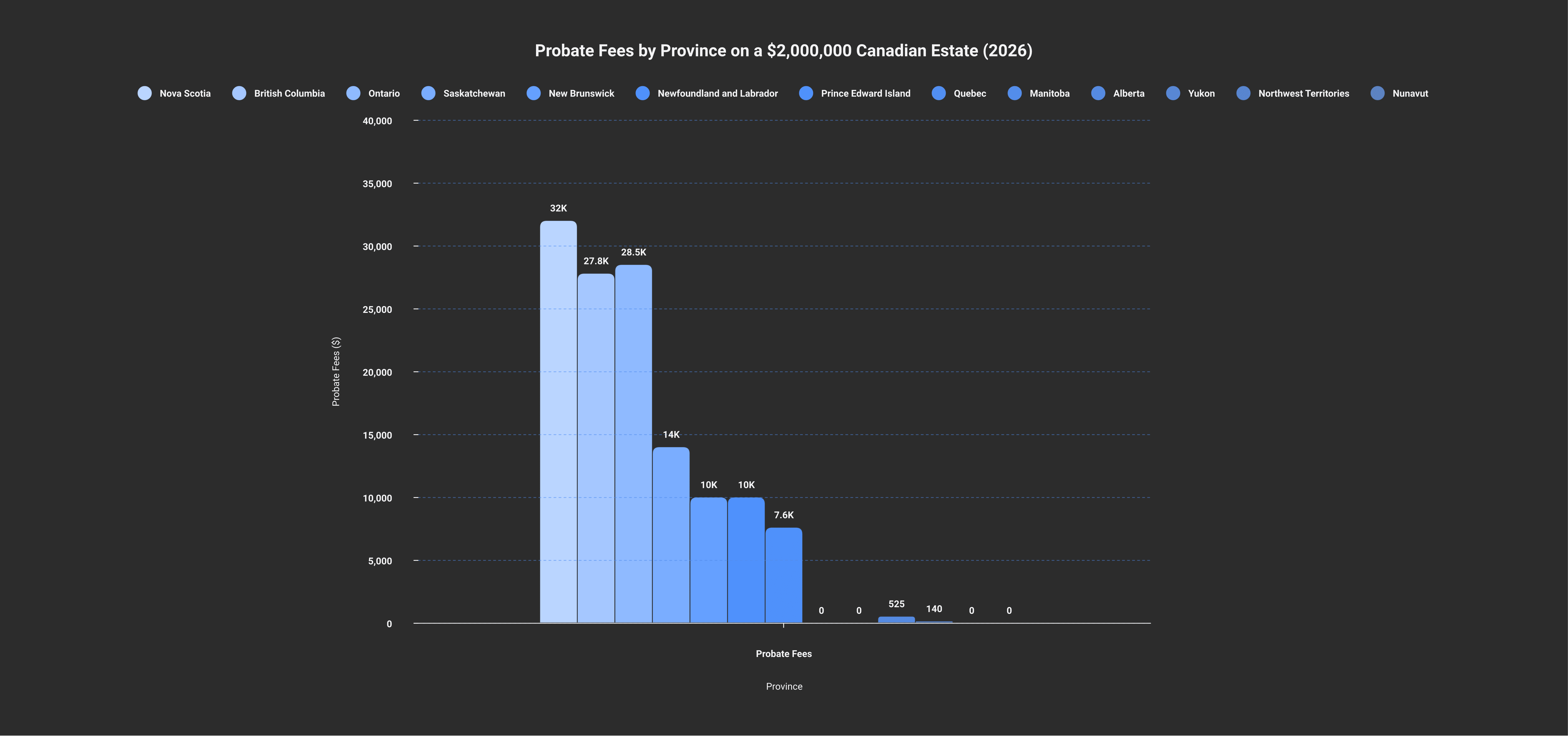

Probate fees by province

Probate fees are a separate provincial levy on the value of the estate, paid to obtain probate (the court's certification that a will is valid and the executor is authorised to act). Probate fees are not income tax. They are calculated on the estate's gross value subject to probate.

Province/Territory | Fee structure | Notes |

|---|---|---|

British Columbia | 0.6% on $25K-$50K, 1.4% above; first $25K exempt | No cap — high-value estates pay the most |

Alberta | Flat fee based on estate size — capped at $525 | Lowest-cost jurisdiction by far |

Saskatchewan | $7 per $1,000 (0.7%) | No cap |

Manitoba | No probate fees (since 2020) | Court fees only ($70-$100 admin) |

Ontario | No tax on first $50K, 1.5% above | Estate Administration Tax — significant for large estates |

Quebec | Generally no fee for notarised wills | Non-notarised wills require a court verification process |

New Brunswick | $5 per $1,000 (0.5%) | No cap |

Nova Scotia | Tiered — approximately 1.7% on portion above $100K | High end |

Prince Edward Island | $4 per $1,000 (0.4%) for portion above $100K | Lower-cost |

Newfoundland and Labrador | 0.5% on first $1K, $0.50 per $1K above | Effectively 0.5% |

Yukon | Flat $140 | No value-based fee |

Northwest Territories | Tiered, modest | Low-cost |

Nunavut | Tiered, modest | Low-cost |

Multi-province estates require probate in each province where real property is located, multiplying the fee.

Planning around probate fees. The most common techniques to reduce the probate base in Ontario and BC (where fees are highest):

Joint tenancy with right of survivorship — property transfers directly to the joint tenant outside the estate. The CRA has scrutinised "intentional" joint tenancies for adult children in Pecore v. Canada (2007 SCC), but the mechanic remains valid for spouses and certain family transfers.

Named beneficiary designations on RRSPs, RRIFs, TFSAs, and life insurance — these transfer outside the estate, avoiding probate fees on their value.

Multiple wills — a primary will for assets requiring probate, a secondary will for shares of private corporations and certain other assets that don't require probate. Established in Ontario by Granovsky Estate v. Ontario (1998).

Inter vivos trusts — moving assets to a trust during the settlor's lifetime so they don't form part of the estate at death.

These techniques can reduce probate fees materially — but each comes with non-tax consequences (loss of control, attribution rules, capital gains triggers on transfer) that should be evaluated alongside the savings.

US estate tax for dual citizens and US persons in Canada

This is where most cross-border estate planning gets complex. The US federal estate tax applies to the worldwide estate of any US citizen, regardless of where they live. It also applies to US-situs assets owned by non-resident aliens (NRAs).

For US citizens (including dual Canadian-US citizens):

The 2026 US federal estate tax exemption is $15 million USD per person ($30M per married couple with portability), permanently set by the One Big Beautiful Bill Act (OBBBA), signed in July 2025. The amount is indexed from 2027.

The OBBBA replaced the previously-scheduled December 31, 2025 sunset of the TCJA exemption (which would have dropped the amount to roughly $7M USD per person). The exemption is now permanent rather than temporary.

For deaths above the exemption, the federal estate tax rate is 40% on the excess.

The Canada-US Tax Treaty provides an "estate tax credit" mechanism (Article XXIX-B) that prorates the US exemption based on the ratio of US-situs assets to worldwide assets. For most Canadian estates, this effectively eliminates US estate tax on US-situs assets below approximately $60,000 USD.

For non-resident aliens (Canadians who are not US citizens) owning US-situs assets:

US estate tax applies to US-situs assets (US real estate, US-domiciled mutual funds and ETFs, US-listed corporate shares held in non-registered accounts) above the small $60,000 USD NRA exemption.

The treaty credit can lift the effective exemption to a prorated portion of the full US exemption.

Common US-situs traps: shares of US companies held in a non-registered Canadian brokerage account, US ETFs (even when held in Canadian-dollar Canadian brokerage accounts).

The cross-border estate tax mechanics warrant their own deep dive. Modern Axis works extensively with US persons living in Canada and Canadians with US tax exposure — the estate planning here is fact-specific and the higher OBBBA exemption changes the calculus for many cross-border estates that were previously sized to the lower pre-OBBBA threshold.

RRSP/RRIF rollover on death — get the beneficiary designation right

A correctly-named beneficiary on an RRSP or RRIF is one of the most consequential pieces of paperwork in a Canadian estate plan. The options:

Surviving spouse named as successor or beneficiary — RRSP/RRIF balance rolls over tax-deferred to the surviving spouse's plan under subsection 60(l). No income on terminal return.

Financially dependent child or grandchild named — rolls over with some restrictions (typically requires the child to have been a dependant for tax purposes), can purchase a term annuity to spread tax over multiple years.

Adult child or grandchild named (not financially dependent) — gets the balance as a lump sum, but the deceased's terminal return includes the full balance as taxable income, often pushing the deceased into the top bracket and creating a tax bill the estate must pay.

Estate named as beneficiary — same as no beneficiary: full balance included in terminal return, distributed by the will.

The mistake: an aging parent with substantial RRSPs leaving them to an adult child. The child receives the full balance, but the parent's terminal return absorbs the income tax — often eating most of the inheritance the child was supposed to receive. Naming the spouse first (if living) and the adult children only as contingent beneficiaries is usually the right structure.

Common myths

"Inheritances over a certain amount are taxed." False. There is no inheritance tax in Canada. The tax has been paid by the estate before distribution.

"Probate fees are inheritance tax." Partially false. Probate fees are a provincial levy on the gross value of the estate, separate from income tax. They are real costs but not "inheritance tax" in the income-tax sense.

"My RRSP goes to my kids tax-free." False (in most cases). Without a spouse named as beneficiary, the RRSP balance is included in the deceased's terminal return as ordinary income. The kids receive the balance, but the tax bill on it is paid out of the estate.

"Joint tenancy with my adult child avoids tax." Partially false. Joint tenancy avoids probate, but the transfer to joint tenancy may trigger an immediate disposition (50% transferred to the child at FMV) — generating a capital gain at the time of joint-tenancy creation. The "tax avoidance" is mostly probate-fee avoidance, not income-tax avoidance.

"Life insurance proceeds are tax-free, so I should use it as an estate tool." Mostly true. Life insurance proceeds paid to a named beneficiary are tax-free under section 148. The capital dividend account generated on receipt by a corporation allows tax-free distribution of the proceeds via a capital dividend. This is genuinely powerful estate planning for owner-managers.

Planning sequence at death

A typical sequence after a death:

Identify the named beneficiaries on every registered account (RRSP, RRIF, TFSA), insurance policy, and pension. These bypass the estate and go directly to the beneficiary.

Value all capital property at fair market value as of the date of death.

Apply the spousal rollover for property transferring to a surviving spouse — no deemed disposition.

Apply the principal residence exemption on the family home (Form T1255 or T2091).

Calculate the deemed capital gains on remaining property — the estate's tax bill.

File the terminal T1 return by the later of April 30 of the following year or six months after death.

Pay the probate fees in each province where real property is located.

Distribute the net estate to beneficiaries per the will.

For dual citizens — file the US Form 706 if the worldwide estate exceeds the US exemption.

For most Canadian estates without cross-border complexity, the work is significant but mechanical. For cross-border estates — where US estate tax, treaty positions, and FBAR/8938 reporting all interact — the planning starts decades earlier. At Modern Axis, we work with cross-border clients on estate planning that coordinates Canadian deemed-disposition mechanics, US estate tax exposure, and the treaty-credit math under Article XXIX-B.

Frequently asked questions

Is there an inheritance tax in Canada?

No. Canada does not have an inheritance tax. Beneficiaries do not pay income tax on inherited cash, property, or other assets received as gifts or bequests. However, the estate of the deceased pays income tax on the deemed disposition of capital property under subsection 70(5) of the Income Tax Act before distribution. The tax has effectively been paid by the estate, but it is not levied on the beneficiary.

What is the deemed disposition rule at death in Canada?

Under subsection 70(5) of the Income Tax Act, all capital property owned by a deceased person is treated as having been sold at fair market value immediately before death. The resulting capital gains are taxed on the deceased's terminal tax return at their marginal rate, with the 50% inclusion rate (the 66.67% inclusion proposal was cancelled in 2025). The estate pays the tax before distributing the remaining assets to beneficiaries.

Does the principal residence get taxed at death in Canada?

Generally no. The principal residence exemption under paragraph 40(2)(b) of the Income Tax Act eliminates the capital gain on the deceased's principal residence at death, provided the executor designates the property on Form T1255 or T2091. If the home was rented out for part of the ownership period, the exemption is prorated, and the partial gain may be taxable. The PRE designation is not automatic — the executor must make the election.

Can my spouse inherit my RRSP without paying tax?

Yes, if you name your spouse as the successor or beneficiary of your RRSP. Under subsection 60(l) of the Income Tax Act, an RRSP balance rolls over to the surviving spouse's RRSP or RRIF on a fully tax-deferred basis. If no spouse is named (or if no beneficiary is named at all), the RRSP balance is included in the deceased's terminal return as ordinary income, often producing a large tax bill the estate must pay.

What is the probate fee for an estate in Ontario or BC?

In Ontario, the Estate Administration Tax is nil on the first $50,000 of estate value and 1.5% on the excess. In BC, no fee is payable on the first $25,000; the fee is 0.6% on the value between $25,000 and $50,000 and 1.4% on the excess over $50,000, with no cap. For a $2 million estate, the probate fee in Ontario is approximately $29,250 and in BC approximately $27,800. Probate fees are provincial levies on the value of the estate, separate from income tax.

Do US citizens living in Canada pay US estate tax?

Yes. The US federal estate tax applies to the worldwide estate of any US citizen, regardless of country of residence. The 2026 exemption is $15 million USD per person ($30M per married couple with portability), permanently set by the One Big Beautiful Bill Act (OBBBA) signed in July 2025. The Canada-US Tax Treaty Article XXIX-B provides a credit mechanism that effectively prorates the US exemption based on the ratio of US-situs assets to worldwide assets, reducing the practical effect for most Canadian-resident US citizens.

How long do I have to file the deceased's terminal tax return?

The terminal T1 return is due by the later of April 30 of the year following death, or six months after the date of death. For example, if a person dies on October 15, 2026, the terminal return is due by April 30, 2027 (the later date — the six-months-after-death rule applies only to deaths between November 1 and December 31). If the person was self-employed, the deadline extends to June 15 of the following year, but any tax owing is still due April 30.

Cross-border tax is fact-specific by nature — citizenship, residency, treaty positions, and prior filings can flip the analysis entirely. This post lays out general principles, not advice for your situation, and it cannot cover every angle that might apply to you. Speak with a Canadian and/or US tax professional who can review your full picture before relying on anything you've read here.

Alex Ataman, CPA

Founder

Modern Axis CPA