BC Foreign Buyer Tax (ABTT): 2026 Guide

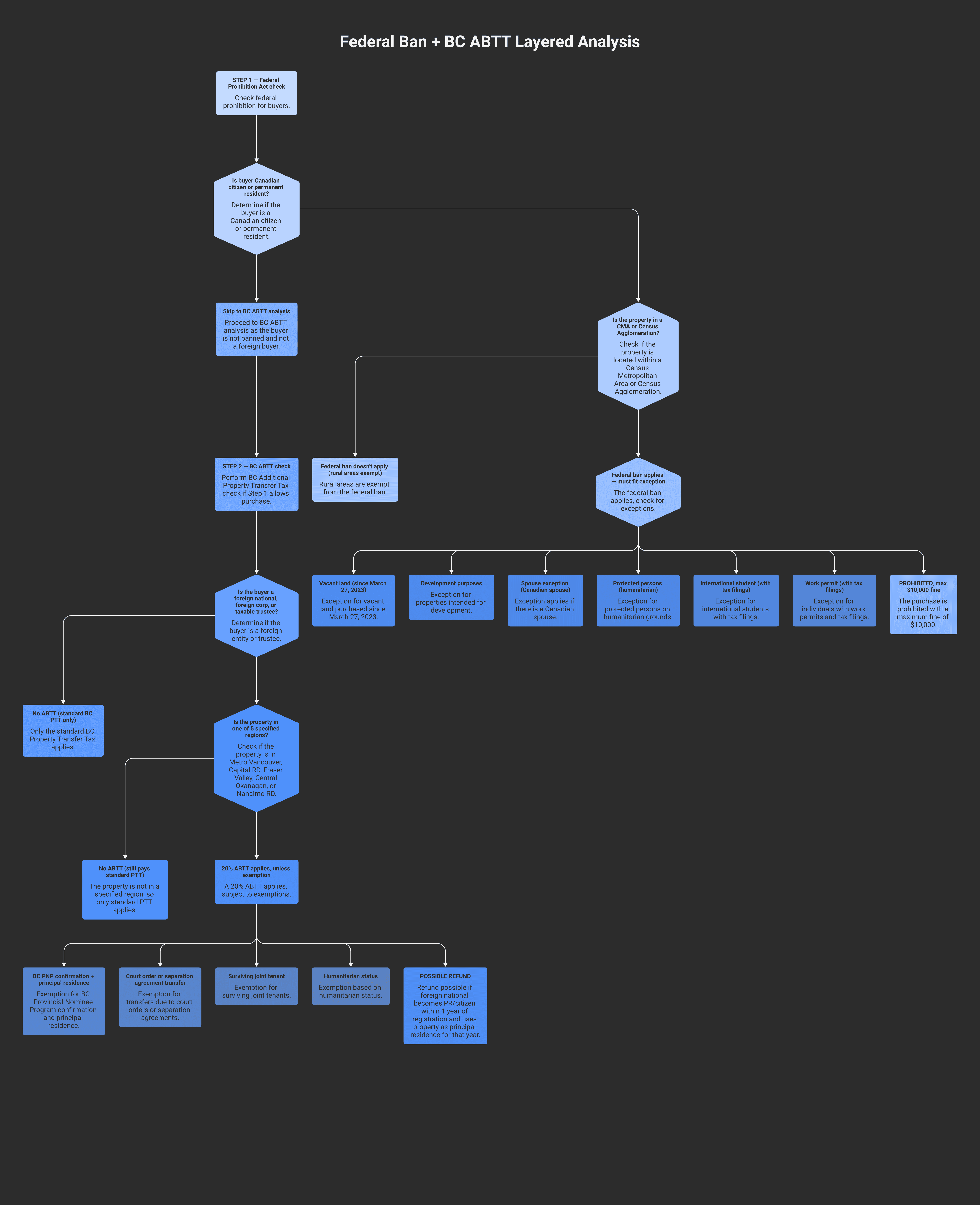

The BC Additional Property Transfer Tax — usually called the "foreign buyer tax" or ABTT — adds 20% of fair market value to the property transfer tax on residential purchases in five specified BC regions by foreign nationals, foreign corporations, and taxable trustees. Combined with the federal Prohibition on the Purchase of Residential Property by Non-Canadians Act (the "federal foreign buyer ban") — which has been extended to January 1, 2027 — most non-resident Canadians cannot purchase residential property in major Canadian cities at all, and where they can, the BC provincial layer applies.

The two regimes are independent and stack uncomfortably for cross-border buyers. The federal ban prohibits a purchase outright in many areas; the BC ABTT adds a 20% tax where the purchase is allowed.

This guide walks through the BC ABTT mechanics — who counts as a foreign buyer, where the tax applies, the available exemptions (PNP, work permit, principal residence rebate), and how it interacts with the federal ban.

Key takeaways

The BC Additional Property Transfer Tax is 20% of fair market value of the residential portion of a property purchased by a foreign national, foreign corporation, or taxable trustee, under sections 2.01 to 2.04 of the BC Property Transfer Tax Act. It applies in addition to the standard BC property transfer tax (PTT).

The tax applies only in five specified regions: Metro Vancouver Regional District, Capital Regional District (Victoria area), Fraser Valley Regional District, Regional District of Central Okanagan (Kelowna), and Regional District of Nanaimo.

Exemptions: foreign nationals confirmed under the BC Provincial Nominee Program (BC PNP) using the property as their principal residence; certain transfers under court order, separation agreement, or to a surviving joint tenant; some humanitarian-status exceptions.

The federal Prohibition on the Purchase of Residential Property by Non-Canadians Act (in force January 1, 2023, extended to January 1, 2027) prohibits non-Canadians from purchasing residential property in Census Metropolitan Areas and Census Agglomerations. Vacant land was carved out March 27, 2023. Maximum fine for breach: $10,000.

A refund of the ABTT is available if the foreign national becomes a permanent resident or Canadian citizen within one year of the property transfer registration, provided the property was used as the principal residence for at least one year.

What is the BC Additional Property Transfer Tax?

The BC Additional Property Transfer Tax (ABTT) was introduced August 2, 2016 at a rate of 15%, then increased to 20% effective February 21, 2018 under the Property Transfer Tax Act. It is layered on top of the standard BC property transfer tax (PTT) — which applies to all property buyers in BC.

The ABTT applies to:

A foreign national (someone who is not a Canadian citizen or permanent resident)

A foreign corporation — a corporation that is not incorporated in Canada, OR a Canadian-incorporated corporation that is controlled by foreign nationals or foreign corporations (per the Property Transfer Tax Act's definition)

A taxable trustee — a foreign national or foreign corporation that holds title as trustee, or a trust where a beneficiary is a foreign national or foreign corporation

The tax is calculated at 20% of the fair market value of the residential portion of the property at the time of registration. Commercial portions and non-residential land are excluded from the calculation.

Where the ABTT applies — the five specified regions

The tax applies only when residential property is transferred in one of these five BC regions:

Region | Cities included |

|---|---|

Metro Vancouver Regional District | Vancouver, Burnaby, Richmond, Surrey, Coquitlam, North/West Vancouver, Delta, New Westminster, Port Coquitlam, Maple Ridge, Pitt Meadows, etc. |

Capital Regional District | Victoria, Saanich, Oak Bay, Esquimalt, Colwood, Langford, Sidney, Sooke, etc. |

Fraser Valley Regional District | Abbotsford, Chilliwack, Mission, Hope, Harrison Hot Springs, Kent |

Regional District of Central Okanagan | Kelowna, West Kelowna, Lake Country, Peachland |

Regional District of Nanaimo | Nanaimo, Parksville, Qualicum Beach, Lantzville |

Properties outside these five regions — most of the Kootenay region, the North, much of Vancouver Island outside Capital and Nanaimo districts, much of the Interior — are not subject to the ABTT. The standard BC PTT still applies on all BC purchases by all buyers; the ABTT layer is the regional add-on.

Who is a "foreign buyer"?

The definition under the Property Transfer Tax Act:

Foreign national — an individual who is not a Canadian citizen or permanent resident. This includes:

Tourists

Visitors

Foreign workers (most are subject to the tax — see PNP exemption below)

Foreign students

Refugees who are not yet permanent residents

Foreign corporation — a corporation that is either:

Not incorporated in Canada, OR

Incorporated in Canada but controlled (directly or indirectly) by foreign nationals or foreign corporations

The "controlled" test catches corporations whose shares are held by non-Canadians, even where the corporation itself was set up under provincial or federal Canadian law. The control test in the Property Transfer Tax Act is independent of the more familiar "controlled" definitions in the Income Tax Act.

Taxable trustee — a trustee that is a foreign national or foreign corporation, OR any trustee of a trust in which a beneficiary is a foreign national or foreign corporation. Even a Canadian-resident trustee can be a "taxable trustee" if any beneficiary is a foreign national. This catches structures where a Canadian-resident trustee holds title for a non-Canadian beneficial owner.

Exemptions and refunds

BC Provincial Nominee Program (BC PNP) exemption. A foreign national who is officially confirmed under the BC PNP — meaning they have a confirmation letter from the BC government — is exempt from the ABTT if they use the property as their principal residence. The exemption must be claimed at the time of registration and is documented on the Property Transfer Tax Return.

Refund within one year (becoming a PR or citizen). If a foreign national paid the ABTT and subsequently becomes a Canadian permanent resident or citizen within one year of the property transfer registration, the ABTT is fully refundable, provided:

The property was used as the principal residence

The application for refund is filed within 18 months of the registration date

The person continuously occupied the property as principal residence for at least one year after registration

Other narrow exemptions:

Transfers under a court order (e.g., a foreclosure to a foreign buyer, or a court-ordered division)

Transfers under a written separation agreement

Transfers to a surviving joint tenant who is a foreign national (provided the transfer is from a Canadian co-owner)

Some humanitarian-grounds residents (refugees who have not yet achieved PR status face complications — see below)

Transfers between spouses (one Canadian, one foreign national) where the property is acquired solely in the Canadian's name (the ABTT typically wouldn't apply at all in this case because the Canadian is the buyer)

No work-permit exemption. A 2018 amendment eliminated the prior "work permit" exemption — foreign nationals on work permits who are not BC PNP-confirmed are subject to the full 20% ABTT.

The federal Prohibition Act — what it adds

The federal Prohibition on the Purchase of Residential Property by Non-Canadians Act came into force January 1, 2023. It prohibits non-Canadians from purchasing certain residential property anywhere in Canada — fully separate from the BC ABTT.

Original term: 2 years (2023-2024). Extended: the prohibition was extended in early 2024 to January 1, 2027.

What's prohibited. Purchase of residential property by a non-Canadian in Census Metropolitan Areas (CMAs) and Census Agglomerations (CAs) — essentially Canadian cities and large towns. Properties outside CMAs/CAs are not subject to the federal ban.

Residential property is defined as: buildings with 3 or fewer dwelling units (single-family, semi-detached, townhouses, condos) and the land they sit on. Buildings with 4 or more units are not subject to the federal ban.

Exceptions (March 27, 2023 amendments) that opened the ban significantly:

Vacant land — no longer covered by the ban (regardless of intended use)

Development purposes — non-Canadians can purchase to develop (build new housing, refurbish, redevelop)

Control threshold — a Canadian corporation is treated as non-Canadian only if foreign-controlled at 10% or more (raised from the original 3%)

Spouse exception — purchase with a Canadian spouse or common-law partner is permitted

Protected persons (some refugees and individuals with humanitarian status)

International students meeting specific residency and tax-filing criteria

Work-permit holders meeting specific residency and tax-filing criteria

Penalty for breach: up to $10,000 per individual involved (the buyer plus anyone who knowingly assisted). The court may also order the sale of the property.

For a foreign national considering purchasing in BC, the analysis is:

Is the property in a CMA or CA? Most of Metro Vancouver, the Capital Region (Victoria), Kelowna, Nanaimo, and Abbotsford-Chilliwack are CMAs or CAs. → Federal ban applies; can they fit an exception (spouse, development, work permit/international student exceptions)?

If allowed federally, is the property in one of the 5 BC specified regions? → BC ABTT applies at 20% unless an exemption (PNP, court order, etc.) applies.

The two regimes catch overlapping but not identical sets of buyers. A foreign national wanting to buy a condo in downtown Vancouver typically faces the federal ban first; even if they can clear it via an exception, the BC ABTT adds 20% on top.

Practical buyer scenarios

Foreign national on a work permit, employed in Vancouver. Federal ban exception for work-permit holders requires only that they have 183 or more days of validity remaining on their work permit or work authorization on the date of purchase, and that they have not already purchased a residential property while the prohibition is in effect (since the March 27, 2023 amendments, there is no tax-filing or physical-presence requirement for work-permit holders). BC ABTT applies in full at 20% (the prior work-permit exemption was eliminated in 2018) — unless the buyer is also confirmed under the BC PNP, in which case the principal-residence exemption applies.

Foreign student studying in Victoria, parents in their home country, scholarship-funded. Federal ban exception for international students may apply if the student has filed Canadian tax returns and meets the residency requirements. BC ABTT applies in full at 20% on any Victoria-area purchase (the Capital Region is a specified region). The PNP route generally doesn't fit student status.

US person living in Canada (PR holder), married to a Canadian. Not a "foreign national" under either regime — Canadian permanent residents are exempt from both the federal ban and the BC ABTT. See our cross-border tax filing guide for the related US/Canadian filing obligations.

Foreign corporation buying for development. Federal ban exception for development purposes — the corporation can purchase. BC ABTT typically applies unless the residential portion is small or other exemptions fit. The control test under the BC PTT Act catches corporations controlled by foreign nationals, even if Canadian-incorporated.

Snowbird family wanting to buy a Whistler condo. Whistler is in the Squamish-Lillooet Regional District — not in the five BC ABTT-specified regions. The BC ABTT does not apply. The federal ban does, because Whistler is in the Squamish-Lillooet CA. Federal exception may be available; BC ABTT is not a concern in Whistler specifically.

Foreign-controlled Canadian holding company. Even though incorporated under Canadian law, if foreign-controlled at 10% or more under the federal regime (since March 27, 2023), and meeting the BC PTT Act's "foreign corporation" control test, both regimes apply. Holding-company structures don't escape either regime by being technically Canadian-incorporated.

Other BC residential tax stacks

A foreign national or non-resident purchasing BC residential property typically faces multiple overlapping tax regimes:

BC Property Transfer Tax (PTT) — base levy on all buyers, on a tiered rate from 1% to 5% based on price

BC Additional Property Transfer Tax (ABTT) — the 20% foreign buyer surcharge covered here

BC Speculation and Vacancy Tax (SVT) — an annual property tax on vacant or out-of-province-owned residential property in specified regions (see our BC Speculation Tax guide — forthcoming)

Federal Underused Housing Tax (UHT) — an annual 1% federal tax on certain vacant residential property; mostly applies to non-Canadian, non-PR owners but with several exemptions

Vancouver Empty Homes Tax — a municipal annual tax on vacant Vancouver residential property at 3% of assessed value (separate from the SVT)

For most non-Canadian buyers facing this stack, the practical question becomes whether the residential purchase makes sense at all. The 20% ABTT alone is often determinative; combined with the annual SVT and UHT for vacant properties, the carrying-cost differential is significant.

Cross-border tax planning at Modern Axis regularly covers the foreign-buyer tax stack for incoming clients — particularly US persons relocating to BC with US-side property considerations, BC PNP-confirmed buyers navigating the PNP refund pathway, and foreign-controlled Canadian corporations needing to assess multi-regime exposure.

Frequently asked questions

What is the BC foreign buyer tax rate?

The BC Additional Property Transfer Tax (the "foreign buyer tax") is 20% of the fair market value of the residential portion of a property purchased by a foreign national, foreign corporation, or taxable trustee in one of five specified BC regions. It is layered on top of the standard BC Property Transfer Tax, which applies to all buyers regardless of citizenship.

Where does the BC foreign buyer tax apply?

The ABTT applies only in five specified BC regions: Metro Vancouver Regional District, Capital Regional District (Victoria area), Fraser Valley Regional District, Regional District of Central Okanagan (Kelowna), and Regional District of Nanaimo. Properties outside these five regions are not subject to the ABTT, although the federal Prohibition on the Purchase of Residential Property by Non-Canadians Act may still prohibit the purchase in any CMA or CA.

Who is exempt from the BC foreign buyer tax?

Foreign nationals officially confirmed under the BC Provincial Nominee Program (BC PNP) using the property as their principal residence are exempt. Other narrow exemptions cover court-ordered transfers, transfers under written separation agreements, transfers to a surviving joint tenant, and some humanitarian-status residents. The work-permit exemption that existed before 2018 was eliminated and is no longer available.

Can I get a refund if I become a permanent resident after paying the ABTT?

Yes. If you paid the BC ABTT as a foreign national and subsequently became a Canadian permanent resident or citizen within one year of the property transfer registration, the tax is fully refundable. You must have used the property as your principal residence for at least one year after registration, and the refund application must be filed within 18 months of the registration date.

What is the federal Prohibition on the Purchase of Residential Property by Non-Canadians Act?

The federal Prohibition Act came into force January 1, 2023 and has been extended to January 1, 2027. It prohibits non-Canadians from purchasing certain residential property in Canadian Census Metropolitan Areas (CMAs) and Census Agglomerations (CAs). Residential property is defined as buildings with 3 or fewer dwelling units. Several exceptions apply: development purchases, vacant land (since March 27, 2023), purchase with a Canadian spouse, work-permit holders with 183 or more days of validity remaining on their permit who have not already bought a property during the prohibition, and international students meeting specific residency criteria. Maximum fine for breach is $10,000.

Does the BC ABTT apply if I'm a Canadian permanent resident?

No. Canadian permanent residents are not "foreign nationals" under the BC Property Transfer Tax Act and are not subject to the ABTT. PR holders pay the standard BC Property Transfer Tax (1% to 5% tiered based on price) but not the 20% surcharge. PR holders are also exempt from the federal Prohibition Act.

Does the BC ABTT apply to commercial property?

No. The ABTT applies only to the residential portion of property purchased. A pure commercial property purchase is not subject to the ABTT. For mixed-use property (e.g., a building with retail on the ground floor and apartments above), the ABTT applies only to the residential portion at FMV. The standard BC Property Transfer Tax still applies to the entire transfer regardless of use.

This article is for general information only and does not constitute professional tax, accounting, or legal advice. Every tax situation is different, and a blog post — no matter how detailed — cannot account for the specific facts that may change the analysis for you. Before acting on anything you've read here, speak with a qualified tax professional about your own circumstances.

Alex Ataman, CPA

Founder

Modern Axis CPA